Free windscreen replacement insurance

Free windscreen replacement can be added to your car insurance policy. Read on for more details.

When you take out a comprehensive car insurance policy, you'll have the option to add 'free windscreen replacement' or 'reduced excess windscreen repair' — or something to that effect anyway.

Essentially, this means that if you need to make a claim for windscreen damage, you can do this without having to pay your standard excess which is typically quite high at $800+. Each insurer may offer something different but there's three main options to choose from.

This means that you won't have to pay any excess when you make a claim for windscreen damage. You can usually make 1 or 2 of these claims per policy year.

Some insurers won't offer 'excess free' replacement, but they'll offer a reduced excess option instead. This means you can pay a reduced excess when you need to make a claim for windscreen damage, rather than paying your full standard excess. What that 'reduced excess' looks like will be agreed upon with your insurer but it's usually around the $50 mark.

The wording here is very important. This means that if your windscreen is damaged and can be repaired then you won't need to pay any excess for this work. But if your windscreen needs to be replaced then an excess would apply. No excess windscreen repair usually exists as an included feature of a comprehensive policy and it exists alongside the option to have a reduced excess for windscreen replacement. So the option to have a reduced windscreen if the event a replacement is needed is still available for you to add to your policy.

"Every day I commute to work via the train so I park in a big commuter carpark. One day I got off the train and found that my car windscreen had been smashed in. Luckily, I had included the excess free windscreen replacement option on my comprehensive car insurance so I was able to get it repaired without costing me a cent. The process was super easy and I was back on the road in no time. I've been really thanking myself for not stinging on cover!"

In short, yes. If you have comprehensive car insurance then you're covered for accidental damage to your car, which includes your windscreen.

To make a claim for windscreen damage though, you'd have to pay your standard excess. Depending on how bad your windscreen damage is, this excess is often more expensive than the cost to repair/replace the windscreen and therefore, not worth making a claim for. I'd suggest getting a few quotes for repairs yourself and seeing if they come out more or less expensive than your excess.

The cost of a replacement windscreen can vary widely. You can expect to pay anywhere from $250 to $400 for common cars like a Holden Commodore or Toyota Corolla. There are plenty of aftermarket windscreens for those models on the market and the labour is pretty straightforward.

However, windscreens for some models are harder to come by or are equipped with specialised sensors. This means you'll end up paying up to $1,000 or more. For example, some newer cars have automatic rain sensors that activate your wipers when they sense rain.

"Reduced excess windscreen cover is a non-negotiable for me when it comes to car insurance. It only costs an extra $50 or so every year but it has the capacity to save me hundreds. I won't miss the $50 it costs to add it on but I would miss the peace of mind it brings me every time a rock flies out of a truck and onto my windscreen while travelling on the highway. It's a no brainer for me."

All the policies below either include windscreen replacement/repairs as standard or can have the feature added as an optional extra.

We currently don't have that product, but here are others to consider:

How we picked theseWe analyse over 30 car insurance products across insurance providers, and rate each one for price and features. We collect up to 36 quotes per product, for male and female drivers in New South Wales, Victoria, Queensland, South Australia, Tasmania and Western Australia. Quotes are collected for 20 year olds, 30 year olds and 60 year olds, assuming an excess of $850 for a 2020 Toyota Corolla 4 door sedan model, with an average 15,000 kms driven each year. While we are not allowed to display actual quotes, our Finder Score aims to serve as an indicative guide to how cost and feature competitive a product might be for you.

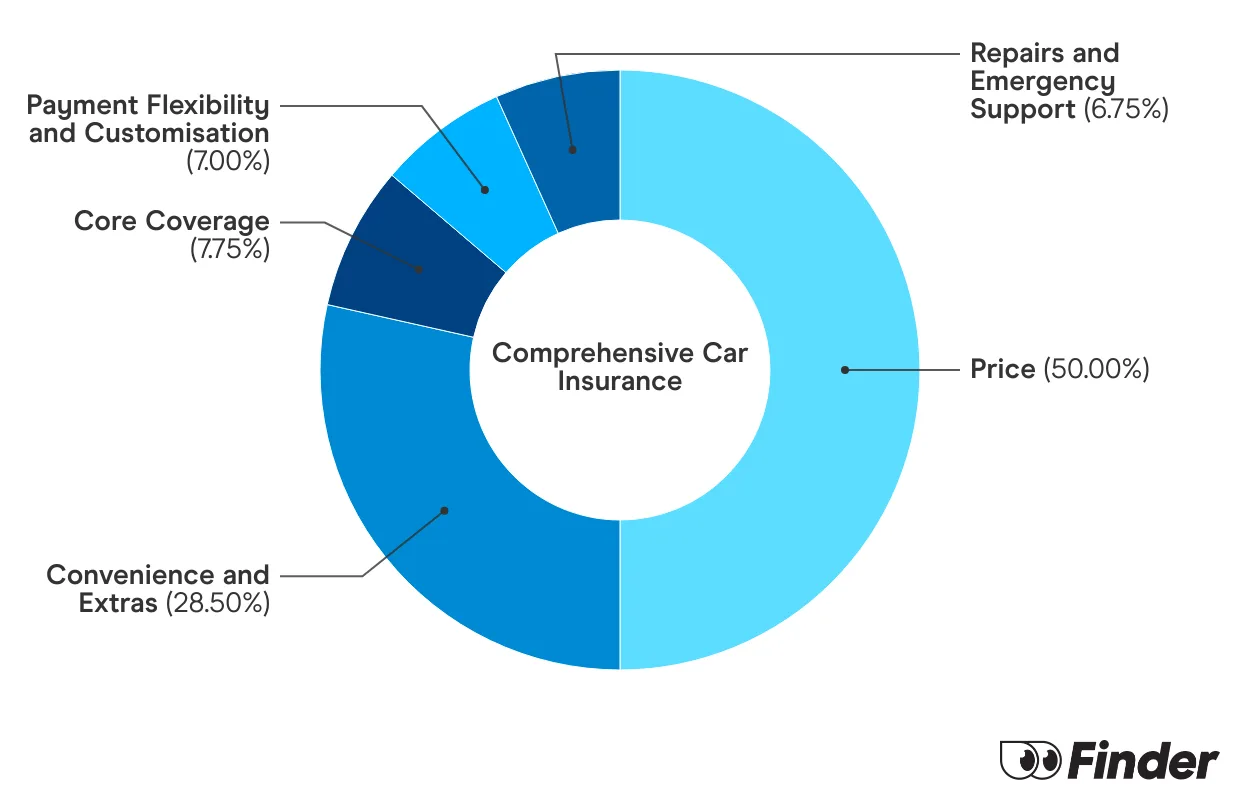

Our feature score assesses each product for more than 15 features across loss and damage coverage, repairs and assistance coverage, personal items coverage and policy coverage. Features we assess include but are not limited to legal liability, essential repairs, new car replacement, car hire events, roadside assistance, agreed or market value, windscreen damage and natural disaster coverage.

Depending on your answers to our car insurance quiz, we upweight the relevant price score or feature score to generate a dynamic Finder Score. Finder Score, Price Score and Feature Score are only to be used as indicative guides and are not product recommendations.

Here's a guide to getting affordable car insurance that will still cover the essentials.

Find out how to get your car registration transferred in Victoria.

NRMA offers 3 levels of roadside assistance. We’ve compared the pricing and features of them all in this article.

Your guide to Blue Slips.

Bank of Queensland car insurance offers three levels of cover, flexible premium payment options and a lifetime guarantee on repairs.

Find affordable and comprehensive car insurance for P-platers with this handy guide.

Compare the latest car insurance discounts and deals to save further on your policy or access bonus offers. Discounts up to 25% for purchasing online

Discover the steps to get affordable car insurance if you are under 25.

Explore our analysis and see how you can find the best car insurance for your needs.

Compare cover from a range of car insurance providers and find out some of the things you will be covered for under a comprehensive policy.