These cards are your ticket to sky-high point earning potential, hefty welcome bonuses, solid ongoing earn rates, and a premium selection of travel-centric perks.

7+

Great

These cards might have slightly less impressive points earning or sign-up bonuses.

5+

Standard

Reliable workhorses for frequent flyers who want a well-balanced card. Enjoy decent point earning potential, competitive rates, and a good mix of practical perks.

0+

Basic

The entry point in the frequent flyer market. Their sign-up bonuses and ongoing earn rates might not be as generous.

How the Finder Score helps you pick the best Qantas card

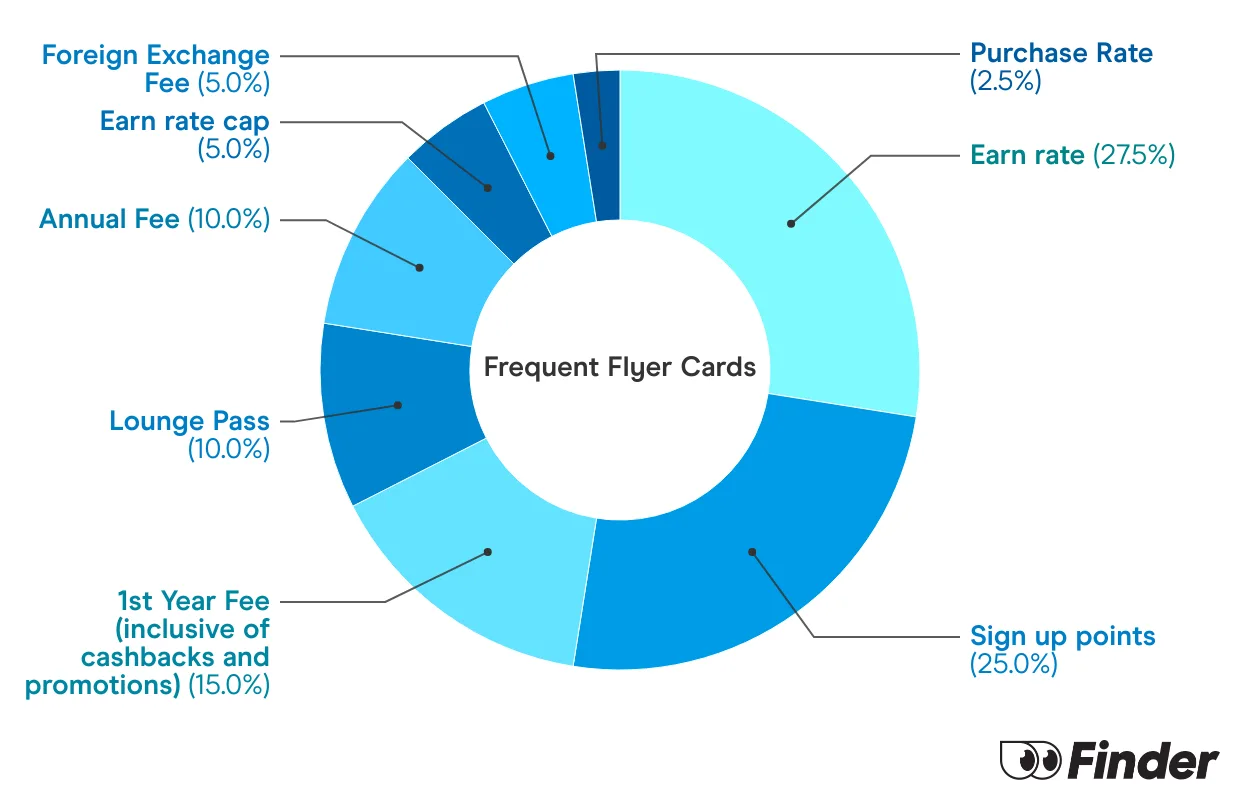

At Finder we do the hard work for you. We've turned hours and hours and hundreds of data points into a simple score out of 10. It's called the Finder Score.

We've scored all our Qantas points-earning credit cards based on the bonus points offer, the earn rate, the perks and benefits, plus card interest rates and fees. The higher a card's the score, the better we think it is for most frequent flyers.

What is the best credit card for Qantas Frequent Flyer Points?

With so many competitive cards on the market, there isn't one best credit card for earning Qantas Points. But you can find a Qantas credit card that works for you based on your frequent flyer goals.

Some of the most popular features to look for include:

Introductory bonus point offers

A high earn rate (e.g. 1 point per $1 or more)

Airport lounge access

Complimentary travel insurance

Flight or travel credit

No annual fee or a reduced annual fee in the first year

If there are other features you want, add them to your comparison (along with the account costs) to find the Qantas credit card that suits you best.

Top frequent flyer credit cards to earn Qantas Points

These are the top scoring Qantas credit cards, based on their Finder Scores.

How can I find the best credit card for earning Qantas Frequent Flyer Points?

When comparing Qantas Frequent Flyer credit cards, it’s important to consider the following factors:

Bonus points offers

These introductory offers can give you thousands of Qantas Points when you get a new card and meet certain requirements. For example, a card might offer 70,000 bonus Qantas Points if you're a new cardholder and spend $3,000 within 3 months of card approval.

How points are earned

These credit cards offer Qantas Points on your everyday spending, which will usually be added to your Qantas Frequent Flyer account once a month. But there are a few different ways this happens, behind the scenes:

Direct earning cards. These Qantas Frequent Flyer credit cards automatically earn Qantas Points as you spend, then deposit them into your frequent flyer account periodically (usually at the end of each statement period).

Cards that let you opt-in to earn Qantas Points. Some reward cards give you the option of earning Qantas Points instead of credit card reward points. Often, you'll pay a yearly fee for choosing the Qantas rewards option on one of these cards. You may also earn a different number of Qantas Points per $1 spent compared to those offered if you earn points through the credit card rewards program.

Qantas Business Rewards. If you get a business credit card that is linked to this frequent flyer program, the Qantas Points you (and your employees) earn will go to a Qantas Business Rewards account. You can then transfer the points to a personal Qantas Frequent Flyer account (or accounts).

Points per $1 spent

Also known as the earn rate, this is how many Qantas Points you'll earn for eligible spending. This usually includes shopping at the supermarket, buying petrol, dining out, paying for holidays and even some bills, although every credit card has different details of what transactions are eligible to earn Qantas Points.

Tip: When comparing earn rates, note that a card may charge a higher annual fee for a higher earn rate. You should always consider if a card's fees are worth its earn rate based on how much you think you'll spend in a year and how many points you would earn.

Points capping

Some cards limit how many points cardholders can earn per $1 spent beyond a spend threshold each statement period.

For example, a card might earn 2 Qantas points per $1 spent up to 6,000 Qantas Points per month and 1 point per $1 for the rest of the month or a maximum of 50,000 Qantas Points in a year.

Interest rates

Frequent flyer credit cards are best suited to people who regularly pay their balance in full each month and avoid interest. This is because these cards usually charge high interest rates, which will quickly outweigh the value of your frequent flyer points.

Annual fee

The cards with the most competitive bonus points offers and features usually have higher annual fees, although some do offer waived annual fees in the first year. A small selection of cards also offer an ongoing $0 annual fee.

Just make sure that the value of the points you're earning and the features you can take advantage of (such as airport lounge passes and flight credits) justify the annual fee.

Extra features

Cards that offer premium perks such as airport lounge passes, travel insurance, personal concierge services or travel credit usually have higher annual fees compared to cards with fewer features.

Carefully consider if these are extras you’ll use and if they justify the higher card cost.

Promoted

American Express Velocity Platinum Card

Earn 70,000 bonus Velocity Points when you apply online by 30 April 2026, are approved, and spend $5,000 on eligible purchases within the first 3 months from card approval and an additional 30,000 points when you spend a minimum of $1 within 90 days of paying your second-year annual fee (up to 100,000 points total).

3 questions to ask before applying for a credit card that earns Qantas Points

Since there’s no perfect credit card that will satisfy everyone’s needs, you should consider your own habits and preferences when choosing your card:

1. How much do I spend on my card?

Think about how often you pay with a credit card. This will help you decide if you can meet the spend requirements to earn bonus points or whether any points caps will restrict your earning potential.

Looking at your usual monthly credit card spending will also give you an idea of how many points you'll earn, what you could redeem with those points and whether that would outweigh the cost of the card's annual fee.

Example: How many Qantas Points would you need to offset a credit card's annual fee?

Let's say you've got a Qantas Frequent Flyer credit card with a $300 annual fee. Based on Finder's Qantas Frequent Flyer Points analysis, you could balance out the card's annual fee by earning 24,000 Qantas Points and redeeming a return economy flight from Sydney to Melbourne. That is a relatively easy flight reward to get and gives you a value of $316 compared to paying for an average Qantas flight.

The amount you'd need to spend on your card would vary depending on the earn rate. As an example:

If your card offered 1 Qantas Point per $1 spent: You'd need to make $24,000 worth of eligible purchases within a year to offset the annual fee. This works out to be around $2,000 per month in credit card spending.

If your card offered 0.5 Qantas Points per $1 spent: You'd need to spend $48,000 per year, or around $4,000 per month to earn enough points for this reward flight.

Bonus point offers are another way to offset the annual fee. And with some cards offering over 80,000 bonus Qantas Points, the value of points could quickly outweigh this cost in the short-term.

Keep in mind that the value of your Qantas Points varies depending on how you redeem them, which can also affect the value you get from your credit card. But the bottom line is that if you don't spend a lot, it will be harder for you to earn enough Qantas Points to justify an annual fee.

2. What credit card purchases earn Qantas Points?

Eligible purchases that earn points usually include your everyday spending, such as groceries, petrol, dining and travel bookings. Transactions that won't typically earn Qantas Points include:

Cash advances. You won’t earn Qantas Points or reward points on ATM withdrawals, foreign currency purchases or gambling transactions.

Credit card repayments or fees. You won't earn points for paying off your credit card balances or credit card fees.

Balance transfers. If you get a Qantas Frequent Flyer card with a 0% balance transfer offer, keep in mind that you won't earn points on the balance you transfer or any repayments.

Government charges. Most cards for personal use don't allow you to earn points on government charges such as Australian Taxation Office (ATO) payments, car registration fees and council rates. If you want to earn points on these types of payments, start by checking out the range of cards that earn points for ATO payments.

BPAY payments. Most lenders won't allow you to earn points for payments made through BPAY.

Check your credit card's reward program terms and conditions or call your provider to find out exactly what types of transactions won't earn points.

3. Is Qantas my favourite airline?

This may be the most important question to ask. There is no incentive or reason to earn Qantas Points with a credit card if you prefer a different airline or frequent flyer program. If that's the case, you can compare other frequent flyer credit cards to find one that will work for you.

When comparing your options, keep your own needs and spending habits in mind so that you aren't swayed by factors that don't matter as much to you. This also helps you pick the right Qantas Frequent Flyer credit card for you.

With over 20 years of experience in property, finance and investment journalism, Sarah is a trusted expert whose insights regularly appear across television, radio, and print media, including Sunrise, ABC News, and Yahoo! Finance. She has previously served as managing editor for Your Investment Property and Australian Broker, and her expert advice has been shared in the media over 3,500 times since 2023 alone. Sarah holds a Bachelor’s degree in Communications and a Tier 1 Generic Knowledge certification, which complies with ASIC standards.

See full bio

Sarah's expertise

Sarah

has written

210

Finder guides across topics including:

Earn KrisFlyer miles on your everyday spending and get introductory bonus points with a credit card linked to the Singapore Airlines frequent flyer program.

Find out if there are any credit card offers that let you earn Qantas Frequent Flyer Status for your eligible spending and learn more about how to reach Silver, Gold or Platinum Qantas status.

From flights and hotel stays to travel packages, gift cards and merchandise, here’s how to make the most of 100,000 Velocity Points based on your lifestyle and goals.

Reward your spending with an air miles credit card and redeem points for your next flight.

Important information about this website

Finder makes money from featured partners, but editorial opinions are our own.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

The information provided by Frankie is general in nature and has been prepared without considering your objectives, financial situation or needs. Frankie may make mistakes so it's important that you review the information before deciding. By messaging Frankie, you agree to our Terms and have read our Privacy Policy.