Health insurance for IVF and fertility treatment

Both Medicare and health insurance for IVF can cut overall costs by thousands

We researched Finder partners to compare the hospital policies that offer cover for IVF and reproductive services (for example other treatments such as GIFT.) The options below have a 12 month waiting period.

| Response | Female | Male |

|---|---|---|

| For pregnancy cover | 3.07% | 1.04% |

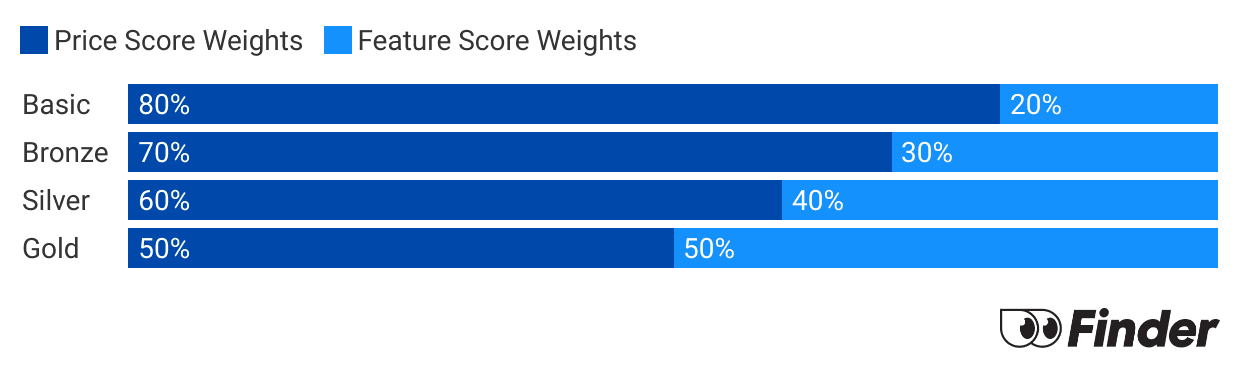

Each month we analyse our hospital insurance products and rate each one on price and features. What we end up with is a nice round number out of 10 that helps you compare hospital cover a bit faster.

Before we start scoring, we need to make sure we're comparing like-for-like. Just as it doesn't make sense to compare a bicycle with a Ferrari, it doesn't make sense to compare basic hospital policies to top-tier Gold policies. Each policy is given a price score and feature score. These are then combined to determine each policies's Finder Score.

All prices are based on a single individual with less than $101,000 income and living in Sydney."My partner and I went through IVF for our first child. We found the treatment was split into two buckets, your IVF specialists costs and the day surgery for the egg retrieval. The whole cycle cost $12,000, the Medicare Rebate offered us the most back at $5000. Insurance did give us a small rebate back of around $1000 but we mostly got the cover for pregnancy should we be successful as both treatments are covered under a Gold Tier policy. There's a 12 month wait period too, so you have to plan early!"

As long as you have a referral from your GP, Medicare will cover a portion of your IVF for as many cycles, or rounds of treatment, as you need. Most IVF centres are privately run and you will have most of your treatment in their private outpatient facilities and, to a lesser extent, their private day hospitals.

Even though it takes place in a private clinic, Medicare will give you a rebate for many aspects of your IVF treatment even if you don't have private health insurance. By the time it's all said and done, your rebates per IVF cycle will be about 50% of the total cost.

All of the services covered by Medicare are listed in the Medicare Benefits Schedule (MBS). The MBS describes the individual inpatient and outpatient services they cover, along with a dollar amount that equals what Medicare will pay for that service in a public facility. This is called the schedule fee.

But since you’ll be in a private facility, they will only pay a portion of the schedule fee, and even then, only for some services (for example, Medicare will help pay for a doctor to collect your eggs, but they won’t pay anything for you to freeze them).

You’ll be responsible the entire cost of services Medicare doesn’t cover, a portion of the cost of services that Medicare only partially covers, and any additional fees or premiums the clinic decides to charge.

Even though Medicare covers a decent chunk of your costs, private health insurance can be an important source of additional cover. Here's where it can help:

A standard IVF cycle can cost anywhere from $9,000 for a normal IVF cycle to $14,000 if you need to have your ovulation induced and you're using a frozen egg (that’s before any refunds or private cover). These rates include consultations, treatments, medications and fees.

The following tables estimate your out-of-pocket costs for one IVF cycle using data from provider IVF Australia.

| Treatment | Total Cost | Medicare rebate | Estimated out-of-pocket costs |

|---|---|---|---|

| Normal IVF cycle | $9,974 | $4,788 | $5,051 |

| Frozen embryo transfer (FET) | $3,797 | $1,391 | $2,354 |

| Ovulation Induction (OI) | $700 | $0 | $700 |

Since IVF isn't always successful the first time around, you may end up going through multiple cycles and that will push your costs even higher. If you end up having multiple cycles in the same calendar year, Medicare may increase your rebate for the rest of the year if your total out-of-pocket expenses have reached a point called the Medicare Safety Net Threshold (MSNT).

| Treatment | Total Cost | Medicare rebate | Estimated out-of-pocket costs |

|---|---|---|---|

| Normal IVF cycle | $9,974 | $5,344 | $4,484 |

| Frozen embryo transfer (FET) | $3,797 | $1,498 | $2,259 |

| Ovulation Induction (OI) | $700 | $0 | $700 |

Source: IVF Australia. Based on prices from 17 Aug 2018

The table below lists the three most common IVF procedures that you could have as an inpatient (usually at your private IVF clinic's day hospital). Private health insurance will pay the amount in the right-most column plus a percentage of any anaesthesia and doctor's fees, per IVF cycle, up to your benefit limit.

Some women have had up to 8+ cycles before falling pregnant, so these contributions from private health insurance can really add up, especially when you combine them with any of the other forms of cover private health offers.

| IVF service | Medicare Item Number | Description | Medicare Schedule Fee | Amount covered by Medicare in a private setting | Amount covered by your private insurance |

|---|---|---|---|---|---|

| Egg collection | 13212 | The doctor collects mature eggs during your menstrual cycle, usually when you're sedated. | $365.50 | $274.15 | $91.35 |

| Transferring embryo to uterus | 13215 | The doctor places the fertilised egg into your uterus. There is usually no pain or sedation required. | $114.60 | $85.95 | $28.65 |

| Preparing frozen embryos | 13218 | For those using fertilised eggs from a previous menstrual cycle, this is the extra prep work needed to get you ready, including thawing the embryo and manipulating your hormones to mimic a menstrual cycle. | $818.35 | $613.80 | $204.55 |

Source: MBS Online, 4 June 2021

Although it is the most well-known, IVF isn't the only form of fertility treatment available. Here are some of the others.

Neither Medicare nor private health insurance will cover the following procedures related to IVF:

If you're considering IVF or other fertility treatment, here are are some questions you should ask any potential clinic:

A single IVF treatment typically costs over $8,000 in Australia. Here’s how Medicare and private health insurance can help.

Your guide to C-sections and how they're covered by private health insurance and Medicare.

Pregnant and unsure whether to have your baby in a public or private hospital? Here’s your guide on how to choose where to give birth.

Want to add your children to your private health insurance policy? Here’s what you need to do.

Make sure your newborn is protected by your health insurance policy.