Compare home and contents insurance

Why compare home and contents insurance? To save money, of course.

We currently don't have that product, but here are others to consider:

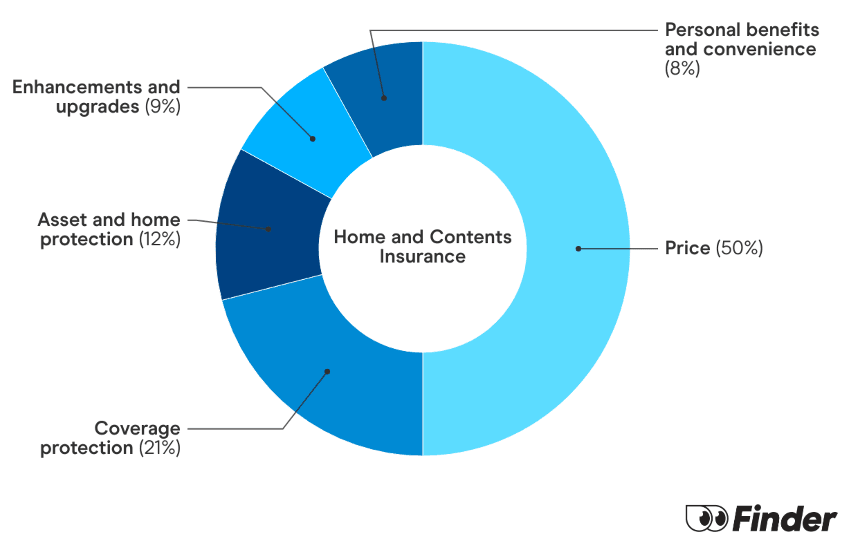

How we picked theseEach month, we get crunching on most every home insurance product in Australia to see how they stack up. We rank over 50 products on 16 different features, including price. We end up with a single score out of 10 that helps you compare home insurance a bit faster.

This covers the physical structure of your home. It also includes any permanent fixtures like air conditioning units and TV satellites.

This covers the cost of your belongings that may have been lost or damaged because of an insured event. It includes things like your entertainment system, furniture and even food.

Getting home and contents cover is a no-brainer. You've probably sacrificed a lot to save up a deposit and pay down your mortgage, so why would you risk losing it all? Here's why it's worth every cent.

Because life happens, and that's okay!

Unexpected things happen and there's nothing we can do about it, but getting a home and contents insurance policy will help you prepare for it.

Because replacing everything will cost you.

Look around you, how much was the sofa you're sitting on? The TV you're staring at? The laptop you're using?

Because it's the smart thing to do.

You've worked hard to become a homeowner. It's probably one of the biggest financial decisions of your life – it makes sense to protect it.

Because it's a small price to pay for peace of mind.

Think about the cost of your home, and all your stuff. The price of a home insurance policy is only a fraction of this.

A home and contents insurance policy will generally cover events that could lead to your financial loss. You can find these events in your product disclosure statement (PDS), but they usually include events like fires, storms, theft and vandalism.

Here are some examples where the right home and contents insurance policy can cover you.

All insurance policies will have general exclusions but they might not be the same. That's why it's important to check over your PDS to make sure you understand what is and what isn't covered under your home and contents insurance policy.

General exclusions can vary between insurers, but here are some common ones.

Many of the individual benefit categories (flood, fire, theft, etc) will have their own individual exclusions, so make sure you're fully across those as they apply to your specific policy.

Icons made by Freepik from www.flaticon.com

Icons made by Freepik, Dave Gandy from www.flaticon.com

Cancelling your home insurance is actually quite simple and you can do it at any time.

It’s possible to get home insurance for an unoccupied home, you just have to let your insurer know.

Access the latest home insurance deals and special offers to save further on your policy.

Find out what renter's insurance is, what it covers and how to find the right policy for your needs.

ShareCover offers flexible insurance options for short-stay hosts and rideshare drivers.

Follow these steps to find affordable home insurance that won't leave you stranded.

Are you looking for CGU Home Insurance? Compare and review your options.

What you need to know about finding the best home insurance for you. Compare policies and learn what questions to ask when researching insurance policies.

Guide to understanding building insurance and what it covers.

Compare home and contents insurance - our research shows you can save up to $1,653 by switching.