Without access to worker’s compensation and other employee sick leave benefits in Australia, you’ll need to find another way to keep the paycheques rolling in when you’re sick or injured. Luckily, from less than $3* a day, you can replace up to 85% of your regular income and use it to keep your business running, put food on the table and pay your bills.

Receive an income protection quote for self-employed workers

Some common questions our self-employed users have

Can I get cover?

The great news is that you can get income protection in most cases. If you’re occupation isn't excluded then you are generally covered as long as you work at least 20 hours per week. We looked at 10 common self-employed occupations to understand how an insurer may consider them:

Occupation

How it's interpreted by an insurer

Carpenter

You can get cover but your premium may be increased. Certain types of carpenters roles will attract a greater increase in premiums e.g. carpet layers.

Accountant

Standard occupation, eligible for cover.

Manager

Standard occupation, eligible for cover.

Doctor

Standard occupation, eligible for cover.

Truck Driver

You can get cover but your premium will most likely be increased. Certain types of truck drivers could be uninsurable e.g. Long distance truck drivers.

Plumber

You can get cover but your premium may be increased. Certain types of plumbing jobs will attract a greater increase in premiums e.g. if you work on a roof.

Project manager

You can get cover but your premium may be increased for certain industries e.g. construction.

Engineer

You can get cover but your premium will most likely be increased. Certain types of engineers could be insurable e.g. Marine engineers.

Electrician

You can get cover but your premium may be increased.

Painter

You can get cover but your premium may be increased.

Sales

In most cases it's standard occupation, eligible for cover. There are some cases where your premiums would increase e.g. Lawnmower sales, deliverables.

How much cover can I get?

Income protection insurance usually covers up to 85% of your regular income. If you don’t know exactly what your income will be for the year then insurers will let you tell them how much you want covered. At claim time you'll need to confirm your income however with proof.

What can I use income protection for?

Income protection generally replaces up to 75% or 85% of your regular income. Payments can be used to:

Keep your business running

Pay the bills of the household

Put food on the table

Help with expenses relating to your care and recovery

What are the key benefits of getting income protection?

Ongoing salary when you can’t work. If you find yourself unable to work because of illness or injury, you can rest easy knowing that you will receive up to 75% or 85% of your income.

Cover for business expenses. If you are a small business owner, you will also have the security of knowing you will be able to keep your business running, particularly if you add business expenses cover to your policy. This takes care of fixed expenses such as office rent, staff salaries, utility bills and even hiring a replacement in your absence.

Additional payment while you recover. Depending on the policy, you may have coverage for additional costs such as rehabilitation expenses, additional benefits for specified injuries and the cost of hiring a professional nurse. This gives you one less thing to stress about and lets you focus on getting better and back to work faster.

Premiums may be tax-deductible. Other benefits of income protection insurance include the ability to recoup some of your premium costs by claiming them back on your tax and being able to fund your IP cover through your superannuation.

Do you qualify for income protection insurance?

Generally, to qualify for income protection you'll meet the following requirements:

You're aged between 18-65

Carry out at least 20 hours of work each week

Have been working in the same occupation for at least 12 months before taking out cover

You're an Australian resident

Can self-employed contract workers get income protection?

Yes, you can generally find cover provided you work at least 20 hours per week and have held the position for at least 12 months.

It's worth comparing options with an adviser to find out what cover options are available.

Workers compensation for self-employed?

Workers' compensation protects an employee if they suffer an injury or illness in the workplace and covers costs such as:

Weekly benefits

Medical and hospital expenses

Rehabilitation expenses

A lump sum payment for death or permanent disability

Self-employed workers don't qualify for workers' compensation in Australia. To be eligible for workers' compensation, you must be in a contract of employment with another person or company. It's the employer who is required by law to take out insurance on behalf of their employees. Because you work for yourself and are your own employer, you're not eligible for workers' compensation, which is why having income protection insurance is so important.

What is considered income for self-employed workers?

Most insurance companies recognise the income for self-employed workers as the income generated by their business or practice through their own personal exertion or activities. This is the case for a self-employed worker, a working director or partner in a partnership. Income does not include:

Should you get agreed value or indemnity value cover?

When choosing an income protection policy, you'll need to consider how your benefit will be determined that is: agreed value or indemnity value. The type of policy you choose will vary depending on your circumstances. Basically, the two types can be described as follows:

Agreed value cover. Agreed value is where your income is verified and agreed upon by you and the insurer at the time of taking out your policy. This means you will know from day one what benefit amount you will receive, regardless of any future fluctuations in your income.

Indemnity value cover. Indemnity value is where your income is verified at the time of making a claim. That means if it has gone down for any reason since you applied for cover, the lesser amount is what your benefit will be calculated on.

As self-employed workers can be more prone to fluctuations in income, taking indemnity value cover can be risky, as there is a real possibility that your income could have been reduced in the lead up to making a claim, meaning you will receive a lesser benefit than you may need to cover your expenses.

For this reason, many self-employed workers opt for the security of agreed value cover, even though it's around 20% more expensive. Some insurers have countered this trend by making indemnity value cover more attractive to the self-employed. They do this by reviewing the insured’s income history over the past three years at the time of making a claim and choosing the 12 months in which they received the most income to calculate the benefit.

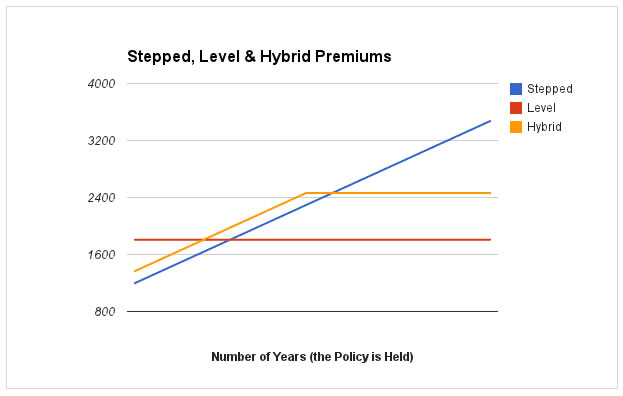

As well as deciding on agreed or indemnity value cover, another important consideration is whether to pay stepped or level premiums.

Stepped premiums. Stepped premiums start out cheaper (calculated on your age at each policy anniversary date) and get progressively more expensive as you get older.

Level premiums. Level premiums are more expensive in the beginning, but because they remain fixed, they become more affordable as time passes (especially after 8 years or more).

When deciding between stepped and level premiums, you need to consider factors such as your age, your budget and the number of years you plan to be self-employed. If you are young and just starting out and are unsure how long you will be running your business, stepped premiums may be a more attractive proposition because they are cheaper.

On the other hand, if you plan to be in business for the long haul, level premiums might be a better option, as despite their initial higher cost, they can save you a considerable amount of money over time.

Another important consideration with IP cover is timeframes, in other words, what benefit period and waiting period?

Benefit period uncovered

The benefit period is the amount of time you receive payments from your insurer. Benefit periods range from two years (the maximum payable within super) to retirement age. Your choice of benefit period will impact your premiums: the longer the benefit period, the higher the cost. However, choosing a longer waiting period might reduce your premiums.

Waiting period uncovered

Waiting periods vary between 14 days and 2 years, so if you think you can survive on sick pay and savings for three months, opting for a waiting period of 90 days would reduce the cost of your premium by about one-third. It’s important to remember though that benefits are always paid a month in arrears, so you will need to factor that into your choice of waiting period.

Your income protection premiums are normally tax deductible. The ATO views any payment you have made or benefits you have claimed that take the place of your regular income as tax deductible, but you can only claim those expenses that are incurred in the generation of assessable income. Any payments or benefits of a capital, private or domestic nature such as accident, illness or death cover in policies like life, trauma and TPD Insurance are not tax deductible.

The amount you get back will depend on your marginal tax rate and it’s important to bear in mind that even though your premiums are tax-deductible, your monthly benefit payments will be assessed (and taxed) as regular income.

Premiums are usually cheaper for members, due to the fund’s ability to buy cover en masse and pass those savings onto its members.

There is minimal impact on your cash flow, as premiums are funded by your super contributions or super account balance.

There is automatic acceptance without the need for medical underwriting.

And the downsides?

There are some disadvantages to funding your IP cover through super and these include:

Only basic cover is provided, with limited features and options (ie. usually no agreed value option, rehabilitation expenses, cancer cover or crisis benefit).

If premiums are funded from your super account balance, your overall retirement savings are being eroded.

Because there is a third party involved (the fund trustee), claims can take longer to be processed.

The claims process can be more complex, with benefits being retained inside the fund unless you satisfy the condition of release under the temporary incapacity definition.

Most policies only pay a benefit for a maximum of two years.

Premiums paid through super are not tax-deductible, unlike policies outside super.

Business expenses insurance: Another option you might want to consider

Business expenses insurance can either be purchased separately or as an additional option on your income protection policy. It covers your fixed business costs while you are off work from injury or illness by paying a monthly reimbursement. This means you can actually focus on your recovery and not mounting debt your business may be facing. Some of the costs that business expenses can help you cover include:

Rent of your office or property that your business uses

Utility bills

Leases on cars and machinery

Staff salaries and superannuation contributions

Building, liability and indemnity insurance

Security costs

Some other key benefits to consider:

Most business expenses policies will pay up to 100% of your allowable business expenses

Premiums are generally tax-deductible

Locum cover is generally provided to cover cost of hiring a replacement worker

Some policies will offer partial payment, when you are partially injured but still able to work at a reduced capacity

Cover generally provided 24 hours a day, worldwide

Most policies will provide up to 75% (in some cases 85%) of your income to a maximum monthly benefit. The maximum benefit is generally around $10,000. This can vary between insurers, as an example Asteron offers a benefit of up to 80%

Most insurers will require you to work a minimum of 20 hours a week to qualify for cover.

You are generally eligible to resume receiving cover without having to undergo a new waiting period if you start your claim again within six months of having returned to work.

Yes. You can increase or decrease your level of cover at any time. Changes are subject to approval from the insurer.

Most policies will require you to be self-employed for up to 12 months prior to taking out cover.

Insurers' class occupations and the risk they present differently. You may be required to pay a higher premium if you are engaged in a high-risk occupation.

Yes, you can receive other compensation/insurance provided the maximum benefit paid does not exceed 75% of your regular income.

Richard Laycock is Finder’s insights editor after spending the last five years writing and editing articles about insurance. His musings can be found across the web including on MoneyMag, Yahoo Finance and Travel Weekly. Richard studied Media at Macquarie University and The Missouri School of Journalism and has a Tier 1 Certification in General Advice for Life Insurance. See full bio

Income protection provides you with income replacement for sickness and illness but not for pregnancy. However, it does offer features to help you out during pregnancy.

NobleOak has been offering personal insurance solutions direct to Australians for over 137 years. Discover the benefits and features available on the NobleOak Income Protection policy and make a secure enquiry for cover.

Compare income protection policies available from OnePath and receive a secure quote from an insurance consultant. Find out how OnePath compares to other insurers.

Looking for the best income protection insurance but not exactly sure where to start? Compare the Finder Awards 2023 insurance winners.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

Important information about this website

finder.com.au is one of Australia's leading comparison websites. We are committed to our readers and stands by our editorial principles

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product. You can learn more about how we make money.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.