- Bessie Hassan

- Head of PR & Money Expert

- finder.com.au

- +61 402 567 568

- Bessie.Hassan@finder.com.au

Media Release

RBA Survey: Smaller banks likely to be the winners from Open Banking – April, 2018

- The Reserve Bank met today and left the cash rate unchanged at 1.50%

- Most panellists (73%) think Open Banking will benefit smaller banks more than the Big Four

- 39% of experts think the Royal Commission may diminish trust among large financial institutions

3 April, 2018, Sydney, Australia – Key events in the financial services sector including Open Banking and the Royal Commission will favour smaller banks over the Big Four, according to exclusive research commissioned by finder.com.au.

This afternoon the Reserve Bank of Australia (RBA) met to discuss monetary policy, and left the cash rate at 1.5% — a decision accurately predicted by all but one member (31/32, 97%) from the finder.com.au RBA survey.

This represents the eighteenth consecutive decision to hold from the board of the RBA.

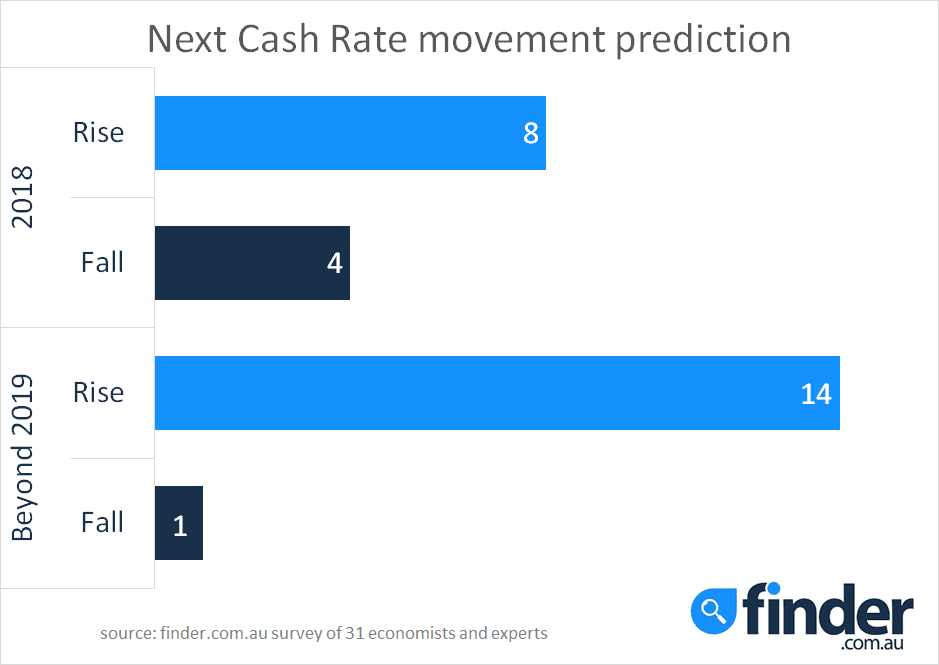

Eight panellists who gave rate forecasts are expecting the cash rate to shift upwards this year.

Interestingly, four experts and economists believe the Reserve Bank will cut the cash rate this year, three of which are predicting a cut in August.

Panellists were asked if data transparency brought about via Open Banking will benefit smaller lenders in Australia more than the Big Four.

Seventy-three percent (11/15) of those who weighed in said Open Banking will favour smaller banks more than it will favour larger financial institutions.

Graham Cooke, Insights Manager at finder.com.au, says Open Banking should drive innovation within the sector.

“It [open banking] should foster competition and promote innovation as banks will be forced to provide a higher level of service to retain and attract customers.

“Switching may become more frequent and we may see customers move away from the larger banks and towards smaller players like credit unions and online lenders.

“More generally, the availability of rich consumer data could lead to the development of smarter and more sophisticated apps to help consumers compare banks,” he says.

The survey asked respondents, “Do you think the Banking Royal Commission is eroding trust in the Big Four, to such a degree that Aussies will increasingly turn to smaller banks and lenders?”

The majority (61%) don’t think the Royal Commission is eroding trust among the Big Four, while 39% (7/18) believe it may erode trust to a point that consumers will refinance to smaller providers.

“As with Open Banking, the Royal Commission will create greater transparency and potentially expose unsavoury practices of certain banks which could hurt their bottom line.

“Misconduct by household names will greatly diminish confidence within the financial services sector, and some Australians may move accounts to smaller lenders if they think larger companies have lost their moral compass,” Mr Cooke says.

Here’s what our experts had to say:

Jordan Eliseo, ABC Bullion (Hold): "The RBA will continue with their current monetary policy settings, though recent data will have dented their confidence regarding the outlook for employment, inflation and overall economic growth. We remain of the view that their next move will be a cut to the cash rate, particularly if house price weakness continues, but this will take time to play out."

Tim Nelson, AGL Energy (Hold): "No material changes to outlook since March. "

Shane Oliver, AMP Capital (Hold): "High business confidence, strong jobs growth and the RBA's own growth and inflation forecasts argue against a rate cut, but risks around consumer spending, weak wages growth and inflation, the slowing Sydney and Melbourne property markets and the still too high $A argue against a rate hike."

Alison Booth, ANU (Hold): "The fundamentals don’t want any change."

John hewson, ANU (Hold): "[The RBA] simply can't move given level of household debt. The economy is still mixed."

Malcolm Wood, Baillieu Holst (Hold): "Inflation below target range, Moderate growth, global volatility."

Paul Dales, Capital Economics (Hold): "There are still no real signs that inflation is heading back up to the middle of the 2-3% target range, so interest rates need to stay low to give it a bit of a boost."

Saul Eslake, Corinna Economic Advisory (Hold): "Nothing has materially changed since the RBA last stated that current monetary policy settings were (in its opinion) appropriate. There’s been no new data on price or wage inflation; and the most recent labour force data suggests that the margin of spare capacity in the labour market remains unchanged, despite ongoing strong employment growth (because most of the new jobs are going to new entrants to the labour force). And the RBA has repeatedly made it clear that it feels under no pressure to follow other central banks in hiking rates."

Peter Gilmore, Gateway Bank (Hold): "The RBA is still concerned about low wages growth and household debt levels."

Mark Brimble, Griffith University (Hold): "Volatility and uncertainty are key factors in the global context and the Australian economy continues to show lackluster performance."

Shane Garrett, Housing Industry Association (Hold): "The current economic environment of strong job creation and fairly weak price pressures does not merit a change in monetary policy from the RBA at this time."

Alex Joiner , IFM Investors (Hold): "There is no material change in the outlook. The labour market continues to perform well however economic activity nor consumer price/wages inflation justifies a near term adjustment of policy."

Michael Witts, ING (Hold): "The RBA will keep rates unchanged as it is looking for the economy to gather further momentum."

Leanne Pilkington, Laing+Simmons (Hold): “The residential housing market, and the economy generally, requires the steady interest rate environment to continue. Employment growth has been encouraging but tempered by flattened wage growth, while house price growth is also subdued and clearance rates are solid if unspectacular. It amounts to a prudent case of the RBA leaving rates as is."

Nicholas Gruen, Lateral Economics (Hold): "The economy has spare capacity and the bank doesn't want to cut – even though for a long time it should have."

Mathew Tiller, LJ Hooker (Hold): "The global economy has continued to show signs of improvement, despite ongoing geopolitical uncertainty. In Australia, the economy remains on a steady footing with business confidence and employment improving. However, this is yet to flow through the increased wages or consumer prices. Housing markets across the country continue to remain active with listings numbers increasing and auction clearance rates sitting just below the long-term average. More properties on the market for sale has provided more choice for buyers and when combined with the moderation of investor demand has led to a slowdown in price growth. In weighing up these variables, it is likely that the RBA will keep the cash rate at the record low of 1.50% over the short-term."

Marie Mortimer, loans.com.au (Hold): "We are speaking to a lot of borrowers who are refinancing with loans.com.au for a cheaper rate than traditional lenders because they are conscious of their household budget. The RBA are also aware of the impact on a rate rise to household budgets and we believe that rates will remain on hold in the short term due to the relatively low inflation rate and weak economic sentiment."

Stephen Koukoulas, Market Economics (Hold): "The RBA is unable to get away from its obsession with non-existent financial instability. It should be cutting rates"

John Caelli, ME (Hold): "The RBA has flagged they are in no hurry in increasing rates. They want to see inflation increase, a pick-up in wages and lower unemployment before they consider putting up rates again."

Michael Yardney, Metropole (Hold): "Despite an increasing divergence with overseas rates, the RBA will keep official rates at their historic low of 1.5% because of spare capacity in our employment markets. While the Australian economy added 17,500 jobs in February, strong population growth and increased labour-force participation meant the official unemployment rate crept up a notch from 5.5% to 5.6%."

Mark Crosby, Monash University (Increase): "Despite ‘The Donald’s’ attempts to trash the world economy, the case for the RBA raising is now very strong."

Christopher Schade, MyState (Hold): "With wages growth subdued and inflation well contained; there is no need for the RBA to rush to raise rates. We would not be surprised to see the RBA on hold for much, if not all of CY 2018."

Alan Oster, nab (Hold): "No increase until we get better wages and more consumer activity."

Jonathan Chancellor, Property Observer (Hold): "More time and confidence is needed before any rate rise."

Matthew Peter, QIC (Hold): "No inflation to speak of, tepid growth, slowing housing market and an unsettled global outlook give the RBA more than enough reasons to remain on hold."

Noel Whittaker, QUT (Hold): "Housing not rising - markets wobbly - no reason to move."

Nerida Conisbee, REA Group (Hold): "Economy still isn't strong enough."

Christine Williams, Smarter Property Investing (Hold): "Unemployment figures have reduced slightly across most states, however individual debt has increased per capita. Banks are continuing to tighten their policy to be in line with responsible lending with owner occupier and investment property loans, thus reducing their overall risk in the property segment."

Besa Deda, St George Bank (Hold): “The inflation outlook does not warrant a near term rate increase from the RBA.”

Brian Parker, Sunsuper (Hold): "Labour market and inflation developments aren't robust enough to warrant any near term tightening, and the RBA is clearly unwilling to ease to boost growth. On hold for a long time!"

Clement Tisdell, UQ-School of Economics (Hold): "No reason for a change."

Bill Evans, Westpac (Hold): "Unlike the “immediate” Trump fiscal stimulus the Australian Government is adopting a more structured, cautious approach."

###

For further information

- Bessie Hassan

- Head of PR & Money Expert

- finder.com.au

- +61 402 567 568

- Bessie.Hassan@finder.com.au

Disclaimer

The information in this release is accurate as of the date published, but rates, fees and other product features may have changed. Please see updated product information on finder.com.au's review pages for the current correct values.

About Finder

Every month 2.6 million unique visitors turn to Finder to save money and time, and to make important life choices. We compare virtually everything from credit cards, phone plans, health insurance, travel deals and much more.

Our free service is 100% independently-owned by three Australians: Fred Schebesta, Frank Restuccia and Jeremy Cabral. Since launching in 2006, Finder has helped Aussies find what they need from 1,800+ brands across 100+ categories.

We continue to expand and launch around the globe, and now have offices in Australia, the United States, the United Kingdom, Canada, Poland and the Philippines. For further information visit www.finder.com.au.

12.6 million average unique monthly audience (June- September 2019), Nielsen Digital Panel