The crème de la crème of personal loans. These products offer the lowest cost loans accompanied by the best features.

7+

Great

Slightly higher in cost and fewer features, but these products are still competitive.

5+

Standard

Typically offering above average rates and possibly lacking in the features department.

0+

Basic

The least competitive in terms of both cost and features.

Key takeaways

Unsecured personal loans don't require collateral, but they often come with higher interest rates

Loan amounts and terms vary, so comparing different lenders can help you find the best option

Approval criteria may be stricter, but funds are typically available quickly once approved.

What is an unsecured personal loan?

With an unsecured personal loan you borrow money without putting up an asset (like a car or property) as security.

You'll get slightly higher interest rates compared to a secured personal loan (where you do offer asset as collateral). That's because if you can't repay the loan there's nothing your lender can repossess and sell to recover your debt - that makes you a higher risk to lend money to.

Unsecured loans can be easier to get though, because secured loans have certain criteria around what you can use as security. And rates can still be competitive.

With an unsecured loan you can borrow anywhere between $2,001 and $100,000 and terms range from 1 to 7 years.

How to compare unsecured personal loans

Look at the interest rate. A lower interest rate makes the loan cheaper. Rates are normally advertised as a range and the better your credit score, the better interest rate you'll get.

Factor in the cost of fees. Some lenders charge hefty fees and in some cases they could cause your loan to cost more than a higher interest rate with no fees.

Choose your loan term and loan amount carefully. The more you borrow the more expensive the loan is. Longer loan terms mean you end up paying more interest. But shorter loan terms make your monthly repayments higher.

Check if the loan allows extra repayments. Most loans let you make extra repayments or pay off the loan early without charging fees, but it's worth checking.

Make sure you're eligible for the loan. Check you meet all the eligibility criteria before submitting an application. You'll need to be over 18, have proof of your income and personal identification documents at a minimum.

The pros and cons of unsecured personal loans

Pros

Fast access to credit. Lenders don't have to assess an asset when you apply for an unsecured loan, so the approval process is faster.

Flexible loan options. These loans have flexible loan terms, loan amounts and often let you make extra repayments easily.

No assets at risk. You don't have to put a car or other asset up as collateral, so there's no risk of repossession, if you can't repay the loan.

Cons

Higher interest rates. While still competitive, the lowest personal loan rates in Australia are almost always going to be secured loans.

Risk of debt and credit score impact. Just because you haven't put up an asset doesn't mean failure to repay the loan won't hurt you. A default will harm your credit score and your lender can still pursue you for the debt in court.

What can I use an unsecured personal loan for?

Unsecured personal loans aren't tied to specific purposes in the way a home loan or a secured car loan is. They're quite flexible, and most lenders don't impose any restrictions on how you use the funds.

Any money you borrow comes with risk if you can't repay it. The best way to minimise those risks is to:

Borrow only what you can afford to repay.

Approaching a reputable, licensed lender (all lenders on Finder are licensed and reputable).

Look at the comparison rate. It factors in the cost of all fees and the loan's interest rate.

The risks of taking out a large personal loan

Borrowing a lot of money is riskier than a small amount, generally speaking. A 5% interest on a small loan won't cost you as much in interest charges as the same rate on a much bigger loan. Here's a simple example:

Loan A

Loan B

Interest rate

12%

12%

Loan term

3 years

3 years

Loan amount

$3,000

$8,000

Total loan cost (loan plus interest)

$3,588

$9,566

These loans are otherwise identical, but the higher loan amount ends up costing the borrower more than $1,500 in interest. Whereas the smaller loan is just $588 of interest.

The risks of taking out a small personal loan

You might think that getting a very small unsecured personal loan is less risky. But if you want to borrow less than $2,000 you probably can't get a personal loan.

Borrowing under $2,000 means you're probably looking at a payday loan. These loans don't have standard interest charges, but come with hefty fees. The price of a small, fast unsecured loan can actually be much higher.

Do unsecured personal loans affect your credit score?

Applying for any loan impacts your credit score temporarily. That's why you should only apply for one product at a time and try to avoid getting your application rejected.

Aside from the initial impact of the application, taking out an unsecured personal loan won't necessarily hurt your credit score. If you make regular repayments and never miss one this will probably benefit your credit score.

Having multiple loans at the same time may hurt your credit score. And debts like credit cards or personal loans can have a bigger impact than something like a home loan.

"Like most personal loans, unsecured personal loans will use your credit score and financial situation to determine your credit rate. So when you're comparing interest rates don't forget that the lowest rate you're seeing might not be the rate you get. You should check your credit score before you apply to understand where you might sit. If your credit score needs improving you can do that by closing or cutting down any existing debt you might have, making sure you pay bills on time and by checking your credit file for any black marks."

Frequently asked questions about unsecured personal loans

Unsecured personal loans are offered both by large, traditional banks such as NAB, and non-bank lenders like OMM or Harmoney. Non-banks are governed by the same regulations as banks, so both are safe and secure options for your borrowing needs.

The key difference between a bank and a non-bank is that non-banks hold a credit licence and not a banking licence. This means that they cannot provide some banking services, such as taking deposits. If you prefer to do all your banking in the same place, you may want to stick to the banks.

Typically, non-banks offer more competitive rates, with lower set-up and ongoing fees. However, they may have fewer loan options compared to traditional banks. Non-banks can also be more flexible and may provide better, personalised service when compared to traditional banks.

Once you have the loan approved, there isn't all that much difference between a personal loan from a big or an online lender. Here are some points to consider:

Online lenders may have lower rates. But the difference is smaller than you think because many banks now have quite competitive rates.

Convenience. The big banks have smartphone apps that make managing your loan easy. If you already bank with one, you could get approved quickly and manage all your savings, cards and loan accounts in one place. But online lenders often have well-designed apps too.

Eligibility. If you have a weak credit score or a history of bad credit then online lenders specialising in personal loans are more likely to have products for you. A bank may decide you're not worth the risk.

Some lenders have no problem with how you use the loan. But some offer specific unsecured business loans and you might be better off getting one of those instead.

If you want to use your business performance in place of proof of income the lender may insist you get a business loan.

Some lenders will happily offer unsecured personal loans to self-employed borrowers, especially if your are able to demonstrate stable income via your business. If this is harder to prove then you could look at a low doc personal loan. These have higher rates but more flexible application criteria.

Unsecured personal loans are relatively easy to get. There's no asset being offered as security, so there's one less thing for the lender to assess. Plus, rates are personalised to your creditworthiness.

But you still need to meet the lender's borrowing requirements.

Most lenders can approve an unsecured personal loan within 24 hours if you meet the lending criteria and have all the identification documents and proof of income.

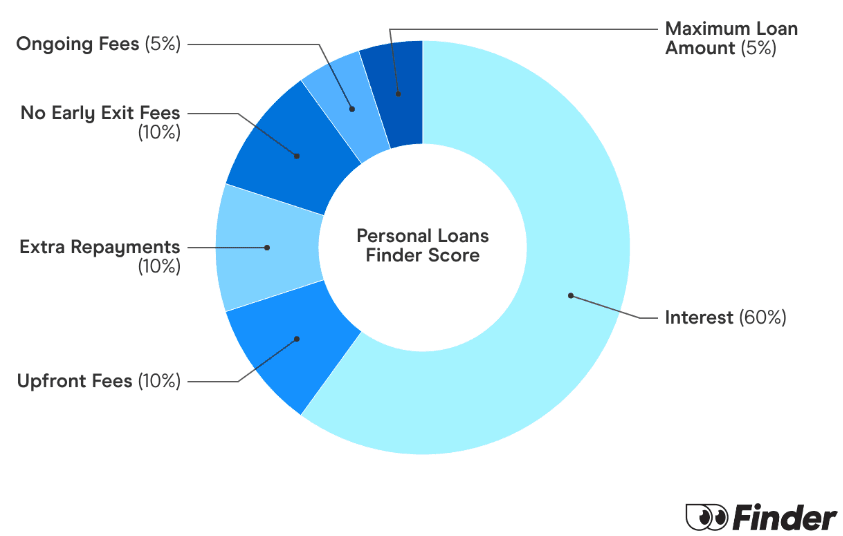

Finder Score for personal loans

To make comparing even easier we came up with the Finder Score. Interest rates, fees and features across 300+ personal loan products and 120+ lenders are all weighted and scaled to produce a score out of 10. The higher the score the better the loan - simple.

For a fair comparison, unsecured loans and secured loans are scored separately. Assumptions are made on the interest rates charged for both excellent credit and average credit customers in each segment.

Addicted to details. We know taking out a personal loan is something you'll be hooked up with for a while. That's why we put hours into research for this guide (and still do at least once a month)

Rates obsessed. Lenders come in all shapes and sizes, that's why we don't just track the big banks, but all the digi folk too. Pretty much everyone but your parents to be honest.

Cash for whatever you need. Lending rates verified from 180+ products day and night. Whether you're buying a car, rennovating your home or heck just ready to let loose with the spending - we got you.

Rebecca Pike is Finder’s money editor, with over 7 years of experience in mortgages and personal finance. A frequent TV and radio commentator, she frequently appears on Sunrise and 7News, Today and 9News, as well as Sky News, Channel 10 and across radio and print. Rebecca previously served as Editor of Mortgage Professional Australia. She has a Master’s degree in Journalism as well as ASIC-recognised certifications in Tier 1 Generic Knowledge and Tier 2 General Advice Deposit Products, which comply with ASIC guidelines.

See full bio

Rebecca's expertise

Rebecca

has written

293

Finder guides across topics including:

I am interested in trying this system out but I am VERY nervous about entering my bank account details online to any site other than the actual bank site. I cannot see any physical street address for Society One and while they may now be part owned by Westpac, i am very dubious about any website that doesn’t list physical address and contact phone numbers ( 1300 doesn’t count ).

So my question is how do I verify the bona fides of the site and satisfy my concerns?

Finder

ShirleyJune 23, 2014Finder

Hi Agsci,

Thanks for your question.

You may be able to source the address of their head office by contacting their customer service team. Similarly, you may be able to obtain a direct number this way.

A lot of banks have a 1300 number as well, but the advantage is that they have physical branches that you can visit if any problems come up. The decision is ultimately up to you as to whether or not you’d like to invest or borrow from SocietyOne.

Cheers,

Shirley

jamieJune 10, 2014

me and my wife want to take a personal loan together to clear our debts

Finder

ShirleyJune 11, 2014Finder

Hi Jamie,

Thanks for your question.

When you’ve found a personal loan you’d like to apply for, please click on ‘apply’.

Remember to check the eligibility requirements beforehand.

Find a low interest loan by comparing your options with Finder. See interest rates, fees, and features for loans across Australia, plus guides to help you get the best deal.

Find out exactly what you need to know when it comes to cheap personal loans, including working out if a loan is really competitive.

Important information about this website

Finder makes money from featured partners, but editorial opinions are our own.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

The information provided by Frankie is general in nature and has been prepared without considering your objectives, financial situation or needs. Frankie may make mistakes so it's important that you review the information before deciding. By messaging Frankie, you agree to our Terms and have read our Privacy Policy.

Addicted to details. We know taking out a personal loan is something you'll be hooked up with for a while. That's why we put hours into research for this guide (and still do at least once a month)

Addicted to details. We know taking out a personal loan is something you'll be hooked up with for a while. That's why we put hours into research for this guide (and still do at least once a month)

Rates obsessed. Lenders come in all shapes and sizes, that's why we don't just track the big banks, but all the digi folk too. Pretty much everyone but your parents to be honest.

Rates obsessed. Lenders come in all shapes and sizes, that's why we don't just track the big banks, but all the digi folk too. Pretty much everyone but your parents to be honest.  Cash for whatever you need. Lending rates verified from 180+ products day and night. Whether you're buying a car, rennovating your home or heck just ready to let loose with the spending - we got you.

Cash for whatever you need. Lending rates verified from 180+ products day and night. Whether you're buying a car, rennovating your home or heck just ready to let loose with the spending - we got you.

I am interested in trying this system out but I am VERY nervous about entering my bank account details online to any site other than the actual bank site. I cannot see any physical street address for Society One and while they may now be part owned by Westpac, i am very dubious about any website that doesn’t list physical address and contact phone numbers ( 1300 doesn’t count ).

So my question is how do I verify the bona fides of the site and satisfy my concerns?

Hi Agsci,

Thanks for your question.

You may be able to source the address of their head office by contacting their customer service team. Similarly, you may be able to obtain a direct number this way.

A lot of banks have a 1300 number as well, but the advantage is that they have physical branches that you can visit if any problems come up. The decision is ultimately up to you as to whether or not you’d like to invest or borrow from SocietyOne.

Cheers,

Shirley

me and my wife want to take a personal loan together to clear our debts

Hi Jamie,

Thanks for your question.

When you’ve found a personal loan you’d like to apply for, please click on ‘apply’.

Remember to check the eligibility requirements beforehand.

Cheers,

Shirley