| Total savings | |

| Total monthly contributions | |

| Interest earned |

Finder makes money from featured partners, but editorial opinions are our own.

A savings account is a secure bank account that earns you interest over time. Unlike an everyday transaction account or standard bank account, a savings account is designed to help you save money rather than use the account for day-to-day transactions and spending. You usually need to deposit a set amount of money into the account each month to earn the high interest rate on your balance, although the conditions do vary between banks.

Bank accounts are designed for your daily spending, and come with a debit card to access your money at shops, ATMs and online. A savings account isn't designed to help you spend, but to help you save, so there's no debit card attached. Savings accounts pay interest on our balance each month, as an incentive to save, while bank accounts typically pay no interest.

It's not an either or situation: you can have both a savings account and a bank account (in fact it's encouraged that you do!).

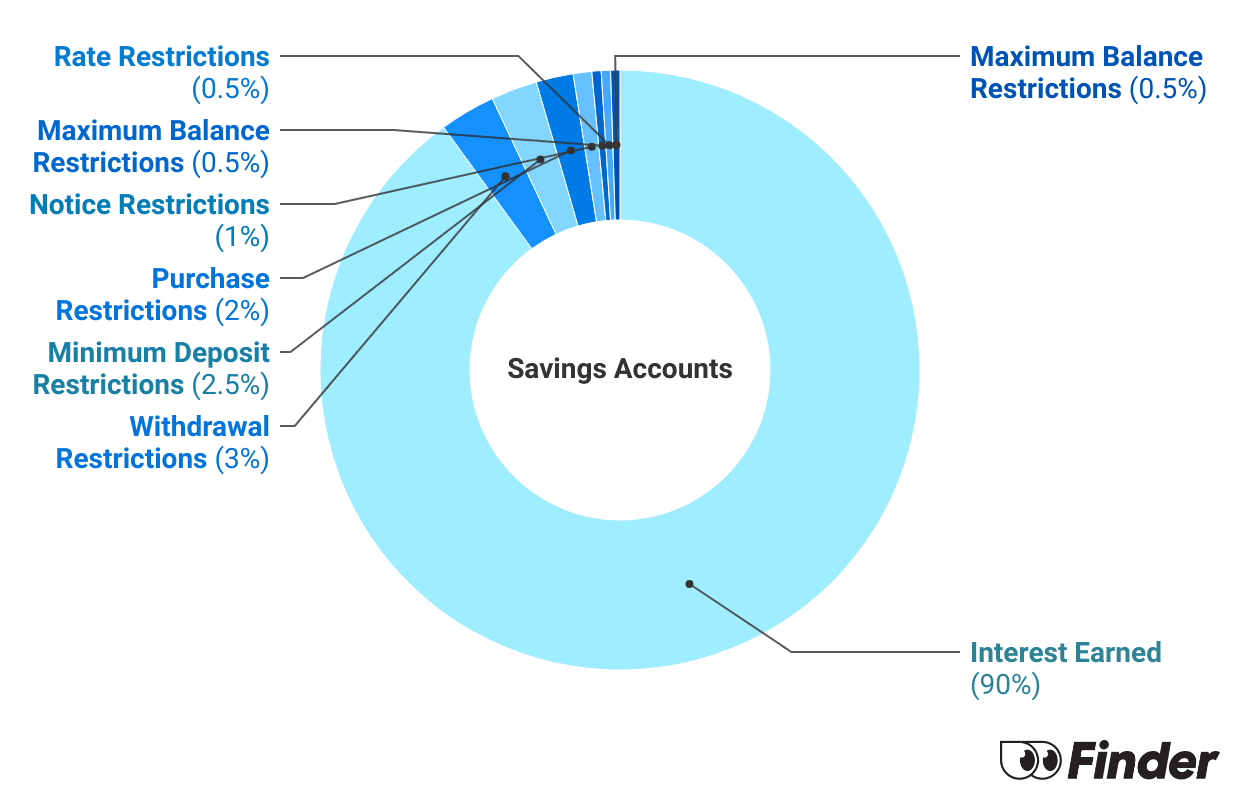

Savings accounts include a couple of different types of interest rates, and understanding how these work will help you in your savings account comparison. Note that the term 'variable' means the rate can change at any time if the bank chooses to change it - it's not a fixed rate.

Thanks to the RBA lifting the official cash rate, we've already seen a number of banks lift their savings rates this year. Even the Big four banks have increased their savings rates, however not by much. The RBA is expected to lift the cash rate several more times this year and next, so we can expect to see savings account rates increase more as well.

Looking at the maximum variable rate is the best way to compare savings accounts, if you're planning to meet all the account conditions to earn it. This is because it's the maximum interest rate you stand to earn. The higher the rate, the more interest you'll earn on your savings.

However, you should take a look at the account conditions too and not the rate on its own. If you don't think you can realistically meet the monthly conditions with one account, you're probably better off going with a savings account with a slightly lower maximum variable rate but conditions you can more easily meet. Because if you can't meet the account conditions you'll only earn the standard variable rate, which is often very low.

See how much you can earn on your savings over time with different interest rates.

| Total savings | |

| Total monthly contributions | |

| Interest earned |

Savings accounts usually don't come with a debit card like everyday transaction accounts, so you can withdraw money from the account at ATMs.

To access the money in your savings account, simply transfer your money from your savings to your linked everyday account using your mobile banking app or via Internet banking. If you've got your bank account and savings account with same bank (this is a good idea!), the money will be transferred instantly which you can then access with your debit card.

Keep in mind that, depending on the savings account you choose, there may be restrictions as to how often you can withdraw from the account before you forfeit your bonus interest. If you know you want to lock away your funds for a longer period, you may want to consider a term deposit instead of a savings account.

There are certain features to keep in mind when comparing savings accounts, including fees, interest rates and your personal savings goals. Read below to find out how these factors can help you compare savings accounts and choose the right one for your needs.

Most banks don't charge a monthly fee for maintaining a savings account. If you're looking at a savings account that does charge a monthly account fee, know that this is not the norm and most accounts have no fees.

Getting the highest interest rate means your money can work harder for you and you'll earn more interest. But you'll want to check the conditions involved in receiving the bonus or introductory rate. If the conditions are too hard for you to meet, there's no point choosing that account as you won't earn the bonus rate anyway.

You might want a different type of savings account depending on your savings goals. If you are saving to buy something in the short term (a few months or a year), high bonus rates and a lower standard rate may be great. However, if you are saving to buy something over the long term (a few years), you might benefit more from an account with slightly lower rates but more manageable, easier conditions to meet.

Some savings accounts allow you to withdraw money a few times each month, while some require you make no withdrawals at all. If you anticipate needing regular access to your savings, you won't want an account that will restrict you for doing so. However, sacrificing bonus interest for accessing your account is also a great incentive for not touching your money and letting it grow. Compared to term deposits, savings accounts offer relatively easy access to your money.

Some banks require you to link your savings account with an everyday account in the same bank to qualify for their interest rate or bonus rate. Even if this isn't a requirement, it's helpful to do so as it'll allow you to see both accounts side-by-side in your mobile banking app. If you do need to get a bank account with the same bank, make sure the bank account doesn't charge high fees.

Some savings accounts will require you deposit just $20 each month in order to earn bonus interest, while others will require much higher monthly deposits (some up to $2000 a month). Choose one that fits in with your ability to save regularly. For example, if you're a casual worker and your income changes a lot month to month meting a larger monthly deposit condition of $2000 might be more challenging.

The type of savings account you choose will depend on the type of saver you are and what you're trying to achieve.

I'm a regular saver: If you can regularly save money each month a bonus saver account with an ongoing bonus rate might be best for you.

I'm just looking for the highest rate: Check out high interest savings accounts (and remember to check the account conditions)

I'm a business owner: There are dedicated business savings accounts for you.

I'm looking for a set-and-forget account with no conditions: Perhaps a term deposit could be suit you better, as these don't have any ongoing conditions to meet and are locked until the term expires.

If you want to make sure your savings account is ethical and aligns with your values, consider the following when choosing an account.

There's a difference between a headline rate and base rate. For an Introductory Bonus account, the bonus interest rate is only awarded for the first couple of months (normally up to 4) and you need to be a new customer.

For a Bonus Saver account, the bonus interest is usually awarded when you're able to deposit a certain amount per month and make no withdrawals. It doesn't matter if you're a new customer or not, but there may be restrictions on the number of accounts you can have.

You will also need to be within the balance your bonus rate applies to. In most cases, any balance beyond $250,000 usually earns the standard variable rate.

It's easy to apply for a savings account online and the process only take 15 minutes. The process involves filling in an online application, verifying 100 points of ID if you're a new customer and depositing funds into the account to get your savings plan started. Items such as a passport or birth certificate are worth 70 points while secondary documents such as driver's licences are worth 40 points. If you already have an account with the same bank you will not have to satisfy the 100-point check.

Not an Australian resident? Don't worry, you can still apply for a savings account if you're an expat or intend to move to Australia permanently.

You'll need the following documents to apply online:

Check out Finder's 5 top Qantas and Velocity Points earning cards on the market this month.

We've ranked them all and found the 5 best balance transfer credit cards on the market.

SPONSORED: Feeling the pinch with your home loan? We touch base with two of the best in the business to find out how you can manage it better.

Millions of Australians are too lazy to return unwanted online purchases, according to new research by Finder.

Millions of Australians have been derailed by an unexpected financial emergency over the past 12 months, according to new research by Finder.

We asked Australians how satisfied they were with their Robo advisor. Here's what they told us.

We asked hundreds Australians how satisfied they were with their share trading platforms. Here's what they told us.

We asked hundreds Australians how satisfied they were with their micro-investing-app. Here's what they told us.

We asked hundreds Australians how satisfied they were with their crypto wallets. Here's what they told us.

We asked hundreds Australians how satisfied they were with their crypto trading platforms. Here's what they told us.