Car insurance for 4WDs

Compare car insurance for your 4x4.

We currently don't have that product, but here are others to consider:

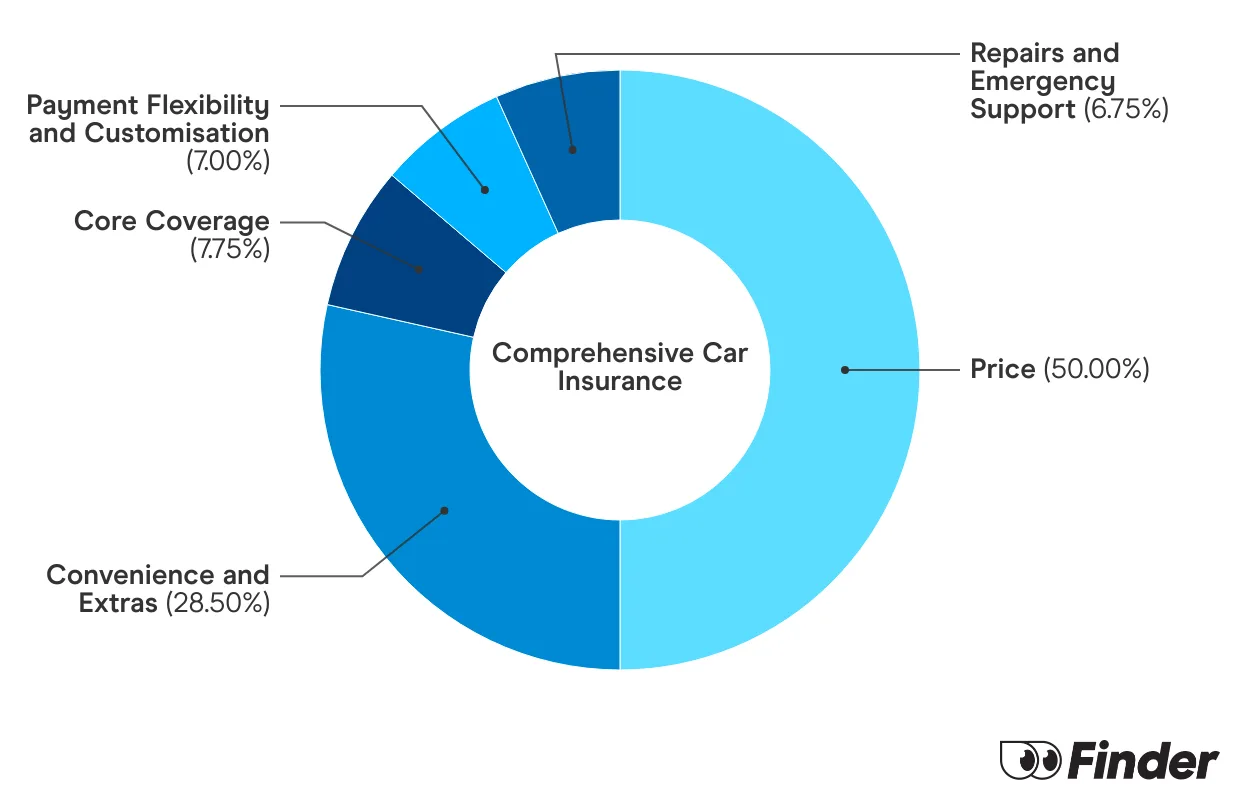

How we picked theseWe analyse over 30 car insurance products across insurance providers, and rate each one for price and features. We collect up to 36 quotes per product, for male and female drivers in New South Wales, Victoria, Queensland, South Australia, Tasmania and Western Australia. Quotes are collected for 20 year olds, 30 year olds and 60 year olds, assuming an excess of $850 for a 2020 Toyota Corolla 4 door sedan model, with an average 15,000 kms driven each year. While we are not allowed to display actual quotes, our Finder Score aims to serve as an indicative guide to how cost and feature competitive a product might be for you.

Our feature score assesses each product for more than 15 features across loss and damage coverage, repairs and assistance coverage, personal items coverage and policy coverage. Features we assess include but are not limited to legal liability, essential repairs, new car replacement, car hire events, roadside assistance, agreed or market value, windscreen damage and natural disaster coverage.

Depending on your answers to our car insurance quiz, we upweight the relevant price score or feature score to generate a dynamic Finder Score. Finder Score, Price Score and Feature Score are only to be used as indicative guides and are not product recommendations.

In many cases, standard car insurance can cover 4x4s. You generally only need to consider specialised 4WD insurance if you want to go off-road or have modified your vehicle. In that case, you’ll need to get the okay from your insurer before you start adventuring.

Specialised off-road car insurance policies are often largely equivalent to comprehensive car insurance with a few additional features. This may include:

Before you can get a quote, you’ll generally need to discuss it with an insurer and do a more in-depth application.

This is not only because of modifications, but also because you generally need to explicitly mention to insurers that you’ll be taking it off road, what kind of driving you do and how frequently you do it.

The optional add-ons available will vary by insurer. If you go with a regular car insurer, you can expect to see the following add-ons:

If you opt for a specialised 4x4 insurer, the optional add-ons are a bit more tailored to off-road activities, such as:

Given off-roading comes with its own set of risks, it’s wise to consider insurance that accounts for this. You might like to look for policies that will:

Here's a guide to getting affordable car insurance that will still cover the essentials.

Find out how to get your car registration transferred in Victoria.

Your guide to Blue Slips.

Your guide to demerit points and how they affect your car insurance.

Bank of Queensland car insurance offers three levels of cover, flexible premium payment options and a lifetime guarantee on repairs.

Find affordable and comprehensive car insurance for P-platers with this handy guide.

Compare the latest car insurance discounts and deals to save further on your policy or access bonus offers. Discounts up to 25% for purchasing online

Discover the steps to get affordable car insurance if you are under 25.

Explore our analysis and see how you can find the best car insurance for your needs.

Compare cover from a range of car insurance providers and find out some of the things you will be covered for under a comprehensive policy.

we were told on the grape vine 4×4 insurance will cover 5wheeler’s we do not take our vechile off road

Hi John,

I would strongly encourage you to speak with your insurer directly before you get behind the wheel so that you know all the types of driving your insurance will cover you for.

Best wishes,

James