Week 2: Understand your debts

Welcome to week 2 of the finder.com.au 12-week financial fitness challenge.

Last week you started to monitor your incomings and outgoings. This week you'll get the complete picture on what you're spending each year, and get on the path to budgeting.

Remember, if you need any help with this week's checklist contact us or tweet to @finderau #12WFFC.

Last week you got a rough idea of what you're spending your money on. This was useful in giving you an idea of how much money you have each month so you can realistically devote yourself to saving, paying off debts and spending.

You're powerless to make a difference to your finances if you don't know your state of affairs first.

This week we're taking what seems like a baby step; however, the outcome is that you'll reduce much of the guesswork that comes with your finances each year. After this week is complete you'll be able to see clearly how much of your salary goes where on an annual basis.

Seeing how much your expenses, hobbies and various addictions cost over a year will help you work out where you can reduce your expenses, or where you can afford to spend more.

Using the information you have from last week, you're going to write up a list of your expenses and go into more detail categorising them into fixed and variable categories.

Fixed expenses are simply expenses which won't change much over the course of a year, and variable expenses are ones that can vary from week to week.

Download the finder.com.au budgeting template

Right click and "Save as"

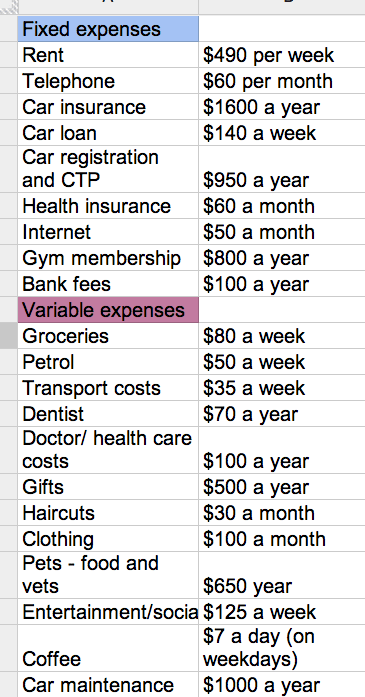

The hypothetical person in this example - let's call him Jim - earns $60,000 a year and is in his mid-20s.

Jim pays rent, has one dog, and is a non-smoker. He also has a car which he's currently paying off with a car loan of approximately $30,000. Jim's goal is to start saving a deposit for a home. Below are the expenses he has over the course of a year.

To create your own table you can make a spreadsheet in Microsoft Excel, Google Docs or just get a piece of paper and a pen.

Start by listing all the expenses you can think of. Some categories such as 'entertainment' might include things such as alcohol or eating out - how you categorise different expenses is up to you.

Once that's complete, simply use the figures you got from week one and multiply them by 52 if they're a weekly expense, 26 if it's a fortnightly expense, or 12 if they're a monthly expense. Some expenses are hard to estimate, and can vary tremendously during each year. If this is the case make a realistic and accurate assumption of what they might cost over a year.

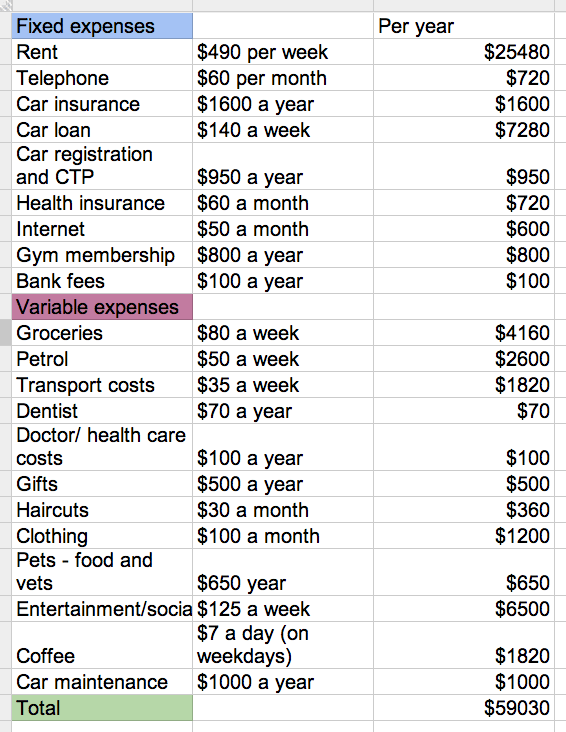

Here's Jim's new expense table:

In the fixed area, note the expenses which won't change or vary much during each year. These can include the examples listed above, or depending on your lifestyle:

The key here is to make the most educated guess you can, and if possible, use the information you received from last week's exercise to help you. For example, you may now have a better idea of what you spend on entertainment each week, so can make an estimate of what your costs will be each week in relation to that.

Expenses relating to health require you to think about your personal circumstances, and if possible look over your bank statements from a longer period than you did last week. If you have a specific health problem, you may need to allow for a larger amount of money each year. In Jim's example we've made an assumption that his health insurance has covered a certain amount of these expenses, and that he hasn't run into any major dental or health problems. This could change, and this brings us to the concept of an emergency account, which we will discuss below.

Other things which may make an appearance in the variable expenses category include:

As you can see from our example, Jim's left with less than $1000 each year which he can use to spend or save, indicating a clear need to cut down on his savings.

If he wanted to put extra money towards his loan and build an emergency account during the year, he'd have to find extra cash.

| Extra towards his loan | $2,000 |

| Emergency account | $1,500 |

| Total required savings | $3,500 |

| Current amount Jim could save | $970 |

| Jim will need to save an extra | $2,530 |

Knowing what he does now after working out his annual expenses, he can identify areas where he can cut down on his spending.

If he eliminated the two coffees he buys each day or switched to homemade coffee – difficult to do, we know – he'd have an instant $1800 or thereabouts to play with. Keep in mind Jim has listed coffee as a variable expense, so the actual amount could fluctuate.

If he reduced his entertainment bill per week to just $100, and bought white-label products rather than premium brands when buying groceries to save a further $15 a week, he could keep as much as $2,000 in his pocket per year.

Together with the coffee this would leave him approximately an extra $3,800 per year which he could split between his loan and an emergency account.

Reducing your expenses will be covered later in the program, but some other ways Jim could start saving right now include finding a cheaper hairdresser; going out one night less per week or shopping around for a cheaper car loan, insurance or other bank accounts.

Almost every personal finance expert will agree that an emergency account is critical to having a successful budget. Having one acts as a buffer against unexpected costs or expenses which blowout over the course of a year.

Having an emergency account means you'll be much less likely to dip into your savings or use a credit card when you run into an unforeseen expense.

No one can tell you how much should be stashed in your emergency account. Some suggest putting aside enough money to cover a few months of your expenses were you to lose your job. Others advocate putting aside enough to get you out of a less serious jam such as a car accident, unexpected bill or other charge, so put the figure between $1,500 - $3,000.

Ultimately you'll need to decide how much you want to have in your account.

Once you establish one, you'll also want to set out how you're going to build your balance. Will you build it as soon as possible or gradually deposit money into an account each month? There are merits to both, and different people will favour different methods.

You should now know where you realistically stand in terms of your income and outgoing expenses. This week's task can be used by anyone, no matter how complicated or simple your finances are. If you pool your finances with your spouse, simply get them to also take part. Next week you'll get into the nuts and bolts of increasing your income. These can help you get off on the right foot whether your goal is to break free of bad debts, start investing, save for a holiday, or whatever else you wish to succeed at.