What we like about the Kogan Money Credit Card - Balance Transfer Offer:

Kogan Money's credit card is a very rare card that combines a genuine ongoing no annual fee with rewards points. This means you not only have a card that costs you nothing to hold, you'll also earn points when you use the card. You can use these points when shopping at Kogan. Just avoid the temptation to buy things you don't need, otherwise your cheap no annual fee credit card will end up costing you more than you planned! It also offers a competitive balance transfer offer and is exclusive to Finder.

Pros & cons

No annual fee

0% p.a. on balance transfers for 18 months

Uncapped reward points

2% balance transfer fee

High 22.74% p.a. interest rate for balance transfers after the introductory period

3.4% foreign currency fee

Best no annual fee cards: Heritage Bank Gold Low Rate Credit Card

The Heritage Bank Gold Low Rate Credit Card has a purchase rate that's lower than most credit cards and an ongoing $0 annual fee, not just a fee waiver for the first year. There's even a balance transfer offer if you're struggling with unpaid card debt.

This card has a Finder Score of 9.34 in the no annual fee category.

Pros & cons

0% p.a. for 12 months on balance transfers

$0 annual fee

Low interest rate of 11.8% p.a. on purchases and cash advances

No interest-free days on purchases

Charges a 3% foreign transaction fee

Best no annual fee cards: American Express Low Rate Credit Card

There is no annual fee for this card at all. It also has a low purchase rate and comes with complimentary card purchase cover.

This card has a Finder Score of 9.47 in the low rate category.

Pros & cons

Low 10.99% p.a. interest rate for purchases

Ongoing $0 annual fee

Complimentary card purchase cover and card refund cover

$30 late payment fee if you miss your minimum repayment

3% foreign currency conversion fee

No rewards program

No annual fee business credit cards

There are a few business credit cards that don't charge an annual fee. At least in the first year. But almost all of them charge an annual fee in the second year, apart from the CommBank Business Low Rate Credit Card, which has a permanent $0 annual fee.

We currently don't have that product, but here are others to consider:

How we picked these

How does a credit card with no annual fee work?

Most credit cards charge an annual fee. No annual fee credit cards don't. Given that annuals fees start from around $50 for low rate cards, and up to $450 or more for frequent flyer cards, you can save a bit with a 0 annual fee credit card.

Some cards charge $0 in the first year only. But right now there are 30 credit cards on the market that charge no annual fee, ever.

Our expert says: No annual fee doesn't mean free

"A $0 annual fee credit card saves you money up front, but make sure you get the most from it. Always pay it off every month in full - once you're paying interest, the card isn't free. And look for other features as well - if you can earn frequent flyer points, you can save real money on travel just by using your card for everyday purchases."

Save money on credit card fees. The most obvious perk of these cards is that you won't pay an annual fee. This could save you tens, hundreds or thousands of dollars over the life of the card.

Practical and cost-effective. A no annual fee credit card can be ideal for emergencies and when extra credit is required. This means you can leave it in your wallet without worrying about it costing you when you're not using it.

Promotional offers and perks. Depending on the card you choose, you can get big bonus points offers, 0% balance transfers and other perks as well as a $0 annual fee for the first year or ongoing.

Cons

Higher interest rates. These cards typically charge higher ongoing interest rates on purchases than some other cards. This could add to your costs if you regularly carry a balance from month to month.

Fewer extra features. While some no annual fee cards do come with rewards and other benefits, they typically boast fewer features than cards with a higher annual fee.

Temporary $0 annual fee. Unfortunately, not all of these cards offer a $0 annual fee for the life of the card. If your card only waives the annual fee for the first year, make sure you know the standard annual fee and when it will apply.

Types of no annual fee credit cards

Some no annual fee credit cards are basic cards for spending that don't offer many perks or extras. But some have balance transfer offers, reward points or complimentary extras.

Earns 0.75 Qantas Points per $1 spent on everyday purchases, 0.5 point / $1 with government bodies in Australia and an additional 1.75 Qantas Point per $1 spent on selected Qantas products and services in Australia, uncapped.

Offers 0% foreign transaction fees overseas and online with international merchants. Plus, complimentary overseas travel insurance.

$0

19.99% p.a.

How to find the right no annual fee credit card

Ask yourself these questions to help compare your options:

How often do you use your credit card? Finder research shows 40% of Australians got their most recent credit card for emergencies. If you rarely use a credit card but want one for unplanned expenses or emergencies, getting one with no annual fee helps you save on costs when you're not using it.

Do you carry a balance? Some no annual fee credit cards have high interest rates that are better suited to cardholders who pay their balance in full each statement period. If you regularly carry a balance, you might want to consider a low interest credit card instead.

Do you have existing debt? You could consider a balance transfer credit card to save money on interest charges for an introductory period. Or, focus on paying off your current debts before you get a new credit card.

Will you use the credit card after a $0 annual fee promotion ends? If it doesn't have a competitive interest rate or extra features to outweigh the cost, you might want to cancel the card before the annual fee kicks in.

What other credit card fees and charges will you pay? As well as interest rates, make sure you check for other credit card fees that could apply, including foreign transaction fees and late payment fees.

Interest-free spending hack

Most credit cards offer a number of interest-free days (such as up to 55) on purchases when you pay your account balance in full by the due date on your statement. So if you pay your account in full, make use of interest-free days and there's no annual fee, your credit card could cost you nothing.

How does the Finder Score work?

To qualify for this category, credit cards must:

Charge no annual fee for at least 12 months.

Every month, we carefully analyse over 250 credit card products and assess the most important features and benefits of each card.

We assign scores out of 10 for each feature, and adjust the scores depending on what category we're looking at.

Credit card scores are category-specific (e.g. No annual fee, Rewards), meaning the same card will receive a different score within each category.

Our Finder Score methodology is designed by our editorial and insights team. Products are reviewed objectively and commercial partners carry no weight. Remember that Finder Score is just one factor to consider. Look at other aspects like fees, features, benefits and risks to make sure a product is suitable for you.

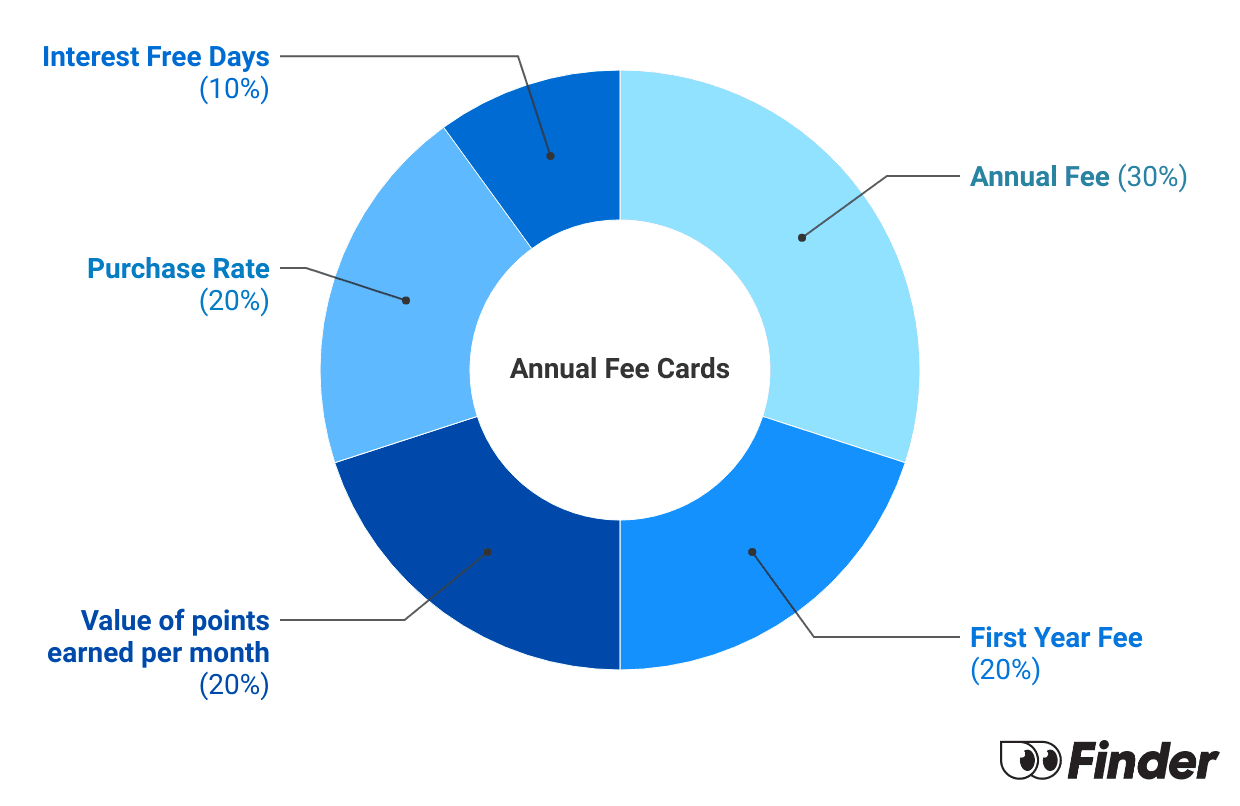

Annual fee credit cards - score weightings

Feature

Definition

Assessment

Weight

Annual Fee

Ongoing fees per year

Lower fees get higher scores, with $0 getting the highest score

30%

First-Year Fee

Introductory fee for the first year

Lower fees get higher scores, with $0 getting the highest score

20%

Interest-Free Days

The number of interest-free days

Higher number of interest-free days score more points, up to 55 days

10%

Value of points earned per month

Points earned for every dollar spent on eligible purchases

Points awarded per dollar

20%

Purchase Rate

Interest rate on new purchases

Lower rates receive higher scores

20%

Finder Score by the numbers

9+ Excellent - These cards offer the lowest ongoing purchase rates, high number of interest free days, and may earn rewards points - all for no annual fee.

7+ Great - Reasonable ongoing purchase rates and interest free days.

5+ Satisfactory - These cards offer no fees, but may have higher interest rates.

Less than 5 – Basic - These are basic cards with no annual fee.

2026 No Annual fee Finder Credit Card Award finalists

While the Finder Scores gives you a real-time ranking of the top credit cards in a category, the Finder Awards recognises the year's consistently high-performing cards. The Finder Credit Card Awards recognises Australia's top credit cards, with expert analysis of rates, fees and offers based on 12 months' worth of data.

The Kogan Money Credit Card is Finder's No Annual Fee Credit Card Winner for 2026. This card not only offers a genuine ongoing no annual fee, it also gives you rewards points on top.

The Kogan Money Credit Card is Finder's No Annual Fee Credit Card Winner for 2026. This card not only offers a genuine ongoing no annual fee, it also gives you rewards points on top.

Heritage Bank's Gold Low Rate Credit Card finished highly commended in the No Annual Fee Credit Card category thanks to its low rate and lack of annual fee.

Heritage Bank's Gold Low Rate Credit Card finished highly commended in the No Annual Fee Credit Card category thanks to its low rate and lack of annual fee.

Qudos Bank's Lifestyle Credit Card ranked highly commended in the No Annual Fee Credit Card category this year with its ongoing $0 annual fee and low rates.

Qudos Bank's Lifestyle Credit Card ranked highly commended in the No Annual Fee Credit Card category this year with its ongoing $0 annual fee and low rates.

Frequently asked questions

If you have a card with a promotional $0 annual fee offer, the annual fee will usually be charged 12 months after you were approved for the credit card.

If you get a credit card that offers no annual fee in the first year, you can cancel it before the annual fee is charged in the second year. Just check your account details online or contact your credit card provider to find out exactly when the annual fee would be charged – and make sure you have paid off the balance – so you can cancel the account before that date.

This depends on the credit card provider. For example, some providers may waive your credit card annual fee when you also take out a home loan package with them. Others may waive or refund your annual fee if you meet specific conditions, such as spending a set amount each year or being a student. You can check the terms and conditions or ask the credit card company to see if an ongoing waiver is possible, or compare cards with ongoing $0 annual fees instead.

If you always pay off your balance in full and can make use of interest-free days on purchases, then a no annual fee card can be very affordable. But if you carry a balance that attracts a high interest rate, the interest charges could make your credit card an expensive option. In this case, you might want to compare credit cards and look at the potential savings you'd get from a card with a low interest rate (even if it has an annual fee).There is no such thing as a "free credit card" because there is always the potential cost of interest if you carry a balance. There are also other credit card fees that may apply for certain transactions (such as cash advances or purchases made in a foreign currency). But in most cases, if you have a $0 annual fee card and pay off your account balance in full by the due date on each statement, you won't be charged interest and can use the card at no cost.

Yes, there are a few no annual fee, low rate credit cards on the market. You can use the filters on Finder's comparison table to narrow down your search based on rates, fees and other features you want. But keep in mind that $0 annual fees and low rates are generally offered on separate cards – except when one of the features is promotional. For example, a $0 annual fee card may offer an introductory low or 0% interest rate before reverting to a higher standard rate, while a low rate credit card could offer a waived annual fee in the first year.

Having a bad credit rating will limit your chances of being approved and getting a credit card, regardless of whether there's an annual fee. You can use our bad credit rating credit card guide to see what credit alternatives are available for applicants with a negative credit history.

Why you can trust Finder's credit card experts

Obsessed with offers - You want all the perks and none of the fees, and we want that for you too. So we're tracking all the current no-fee cards, in one handy guide.

Save yourself some time. Why waste 100s of hours researching no-fee credit cards, when we've done the hard yards for you? Simply sit back, sort the options and get the card that suits your needs

No BS. We'll explain how all the credit card fees work and how you can avoid interest – and we'll always explain it all in plain English.

Richard Whitten is Finder’s Senior Money Editor, with over eight years of experience in home loans, property, credit cards and personal finance. His insights appear in top media outlets like Yahoo Finance, Money Magazine, and the Herald Sun, and he frequently offers expert commentary on television and radio, helping Australians navigate mortgages and property ownership. Richard started his career in education and textbook publishing in South Korea. He holds multiple industry certifications, including a Certificate IV in Mortgage Broking (RG 206) and Tier 1 and Tier 2 certifications (RG 146), as well as a Bachelor of Education from the University of Sydney and a Graduate Certificate in Communications from Deakin University.

See full bio

Richard's expertise

Richard

has written

698

Finder guides across topics including:

who is the best bank/provider if iam on a disability pension ? own my own house ,have a good credit rating.I also receive payments from an accident etc etc?

Finder

RichardJanuary 12, 2026Finder

Hello Inge,

Unfortunately it’s not really possible to say which bank or card company is best someone on a disability pension. You’d need to look for suitable cards and then look at the eligibility criteria before applying.

Sorry I can’t be more helpful.

susanDecember 4, 2025

Would I be able to get a credit card I am on dpp

Finder

SarahDecember 4, 2025Finder

Hi Susan, You may be eligible, depending on the specifics of your situation. You can read more about getting a credit card when you’re on the pension here, and credit cards for people on Centrelink here. Hope this helps!

RobJune 23, 2025

Hi I currently have a Me credit card of $5000 Frank/ Me are going to cancel card in July but still paying balance also a Zippay card $2500

Question would I be better off finding a balance transfer credit card card to bring into 1 card less hassle

Finder

RichardJune 25, 2025Finder

Hi Rob,

A balance transfer will save you money if the interest charges (and card fees) on your 2 cards are higher than what the new balance transfer card will charge.

Assuming you have a combined $7,500 unpaid balance on two cards, you could put that onto a balance transfer card with a 0% offer for 24 months. That gives you 24 months to pay that off with no interest charges.

Annual fees on your old card (versus the annual fee on a new balance transfer card).

The interest charges on your old cards each month.

The balance transfer fee. This is usually 1% to 3% of your balance. 3% of $7,500 is $225, so it’s a big fee.

You also need to think about how long you’ll take to repay the card balance. How much can you put aside each month? After a balance transfer period ends you get charged high interest on any money you still have to repay on the card.

martinDecember 8, 2024

I currently have a credit card and always pay it off monthly. I have noted that purchases attract a %levy of extra money on each purchase. what card should I have to avoid this . I am not interested in rewards/gifts/points of any description but I would like to make online or even international purchases from time to time. I currently do have a debit card from my anz bank for ATM cash but nothing else. could I use that?

Finder

RichardDecember 10, 2024Finder

Hi Martin,

You may want a card with 0% foreign transaction fees for overseas spending. I am not sure what you mean by the % levy on each purchase. If you pay the balance in full each month most cards offer interest free days (up to 45 or 55 days in many cases).

FranAugust 8, 2024

Latitude has just informed me that they are introducing a card fee of $8 per month from September 2024. What is the best credit card option now for travel o/s to avoid the international transaction fees but still have no card fees? I already have the debit card situation sorted.

Make the most of credit cards offering $0 annual fee in the first year and learn about other ways to save on this yearly cost with this guide to annual fees.

Share your credit card with a partner or family member but watch for extra costs. Compare cards and learn more about credit cards that offer free additional cardholders.

Compare no annual fee rewards credit cards and earn points on all eligible purchases without paying a yearly fee.

Important information about this website

Finder makes money from featured partners, but editorial opinions are our own.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

The information provided by Frankie is general in nature and has been prepared without considering your objectives, financial situation or needs. Frankie may make mistakes so it's important that you review the information before deciding. By messaging Frankie, you agree to our Terms and have read our Privacy Policy.

Obsessed with offers - You want all the perks and none of the fees, and we want that for you too. So we're tracking all the current no-fee cards, in one handy guide.

Obsessed with offers - You want all the perks and none of the fees, and we want that for you too. So we're tracking all the current no-fee cards, in one handy guide.

Save yourself some time. Why waste 100s of hours researching no-fee credit cards, when we've done the hard yards for you? Simply sit back, sort the options and get the card that suits your needs

Save yourself some time. Why waste 100s of hours researching no-fee credit cards, when we've done the hard yards for you? Simply sit back, sort the options and get the card that suits your needs

No BS. We'll explain how all the credit card fees work and how you can avoid interest – and we'll always explain it all in plain English.

No BS. We'll explain how all the credit card fees work and how you can avoid interest – and we'll always explain it all in plain English.

who is the best bank/provider if iam on a disability pension ? own my own house ,have a good credit rating.I also receive payments from an accident etc etc?

Hello Inge,

Unfortunately it’s not really possible to say which bank or card company is best someone on a disability pension. You’d need to look for suitable cards and then look at the eligibility criteria before applying.

Sorry I can’t be more helpful.

Would I be able to get a credit card I am on dpp

Hi Susan, You may be eligible, depending on the specifics of your situation. You can read more about getting a credit card when you’re on the pension here, and credit cards for people on Centrelink here. Hope this helps!

Hi I currently have a Me credit card of $5000 Frank/ Me are going to cancel card in July but still paying balance also a Zippay card $2500

Question would I be better off finding a balance transfer credit card card to bring into 1 card less hassle

Hi Rob,

A balance transfer will save you money if the interest charges (and card fees) on your 2 cards are higher than what the new balance transfer card will charge.

Assuming you have a combined $7,500 unpaid balance on two cards, you could put that onto a balance transfer card with a 0% offer for 24 months. That gives you 24 months to pay that off with no interest charges.

We have a calculator here you can use.

Here are the costs you need to consider:

Annual fees on your old card (versus the annual fee on a new balance transfer card).

The interest charges on your old cards each month.

The balance transfer fee. This is usually 1% to 3% of your balance. 3% of $7,500 is $225, so it’s a big fee.

You also need to think about how long you’ll take to repay the card balance. How much can you put aside each month? After a balance transfer period ends you get charged high interest on any money you still have to repay on the card.

I currently have a credit card and always pay it off monthly. I have noted that purchases attract a %levy of extra money on each purchase. what card should I have to avoid this . I am not interested in rewards/gifts/points of any description but I would like to make online or even international purchases from time to time. I currently do have a debit card from my anz bank for ATM cash but nothing else. could I use that?

Hi Martin,

You may want a card with 0% foreign transaction fees for overseas spending. I am not sure what you mean by the % levy on each purchase. If you pay the balance in full each month most cards offer interest free days (up to 45 or 55 days in many cases).

Latitude has just informed me that they are introducing a card fee of $8 per month from September 2024. What is the best credit card option now for travel o/s to avoid the international transaction fees but still have no card fees? I already have the debit card situation sorted.

Hi Fran,

You can review a range of options here.

Hope this helps!