Do you run a business from home?

You might find our guide to insuring a home-based business more useful.

If you're one of the many Australians working from home on a more permanent basis, you should consider home office insurance. It can cover your office appliances and equipment, from monitors to memorabilia, and it's available with certain comprehensive home insurance policies — we've made a list of who below.

Here's a list of the providers who offer home office insurance. Our table doesn't include prices because quotes are based on your specific circumstances, such as the value of your house and the contents inside it. Compare features first, then you can click through to get a personalised quote.

We currently don't have that product, but here are others to consider:

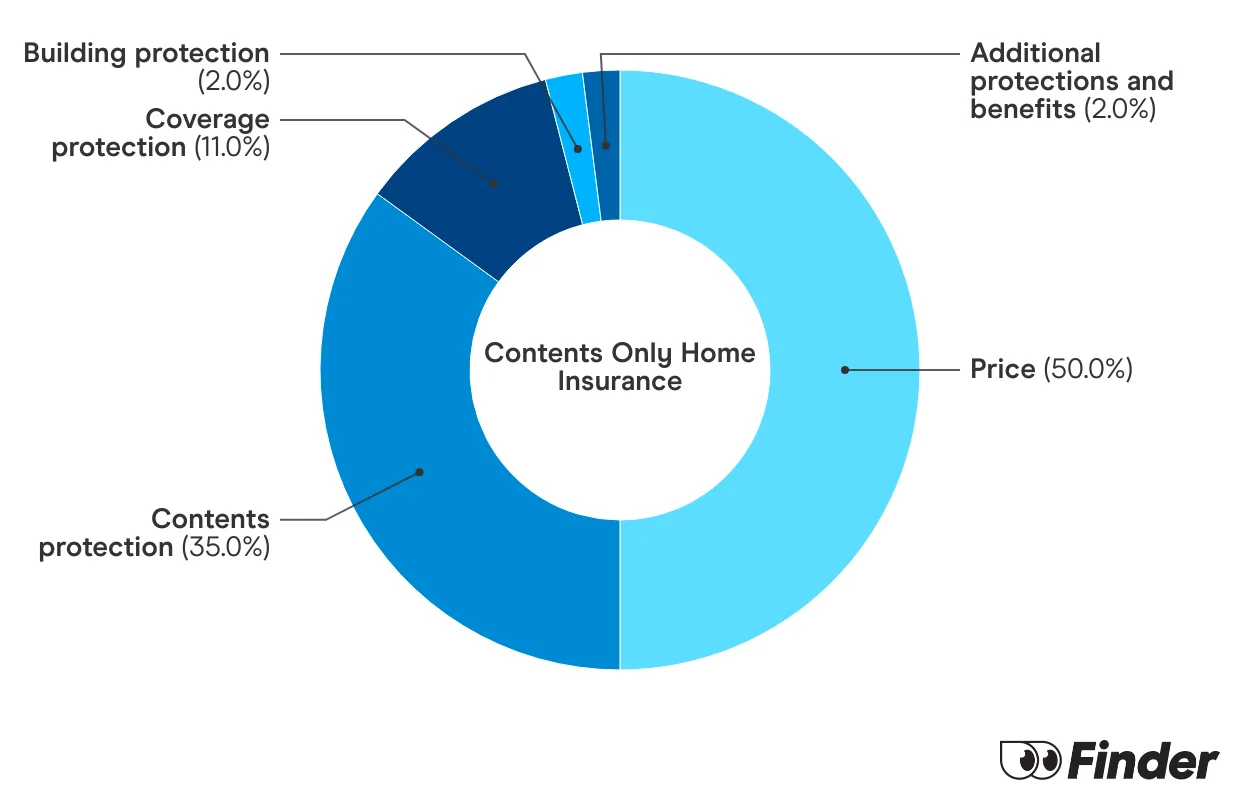

How we picked theseWe crunch eligible home insurance products in Australia to see how they stack up. We rank over 50 products on 16 different features, including price. We end up with a single score out of 10 that helps you compare home insurance a bit faster. We assess home and contents, building only and contents only products individually.

You can get home office insurance with a home and contents insurance policy.

If you have a home office, it can cover clerical items kept in your home. This can include computers, chairs, monitors, headsets, keyboards and other bits and pieces you use to get on with your day job.

It'll be covered under the contents section of your policy, just make sure to check the cover limit.

Here are the home office items that can be covered by a home insurance policy.

You might find our guide to insuring a home-based business more useful.

Yes, it can. If you keep your tools at home, like in a home office or garage, contents insurance can cover you up to a certain amount (often between $1,000 and $5,000) if you get it included under home office insurance. Keep in mind that this only applies when you keep them at home. If you want to get cover for outside the home, you'll need to look for a home and contents insurance policy that allows you to add portable contents cover. You can find out more about insuring tools of trade here.

Household accidents are common. Here's some reasons it might be worth adding accidental damage cover to your policy:

Personal effects cover is for portable items that can be taken away from the home. It's a good idea to get if you also take some of your home office appliances out with you.

There are two types of cover: unspecified personal effects and specified personal effects. Both can protect against accidental loss or damage to a wide range of portable items including cameras, bags, headsets, glasses, laptops and other equipment you use for work.

With the former, you don't need to list the items; you simply choose an individual item limit and a total claim limit. However, you need to list the items with specified personal effects and you can protect them individually for an agreed amount. Taking into consideration your home office equipment,

Every policy has exclusions. With home office insurance, you'll probably find that you won't be covered for:

With so many of us adapted to the new normal of working from home, it's a good idea to update your home insurance policy to ensure your home office is also covered.

Shed insurance can cover sheds of all shapes and sizes, as well as their often-valuable contents.

Find out how home insurance can cover water damage and how to avoid some of the pitfalls.

Cancelling your home insurance is actually quite simple and you can do it at any time.

It’s possible to get home insurance for an unoccupied home, you just have to let your insurer know.

Motor burnout covers those big appliances in your home in the event that they let you down. This article will show you what it is, why it's important and how much it can cost you.

Find out what renter's insurance is, what it covers and how to find the right policy for your needs.

Follow these steps to find affordable home insurance that won't leave you stranded.

What you need to know about finding the best home insurance for you. Compare policies and learn what questions to ask when researching insurance policies.

Building insurance covers your home structure only, not the contents inside. Learn more about what is covered, what isn’t covered and compare your options today.

Compare home and contents insurance - our research shows you can save up to $1,653 by switching.