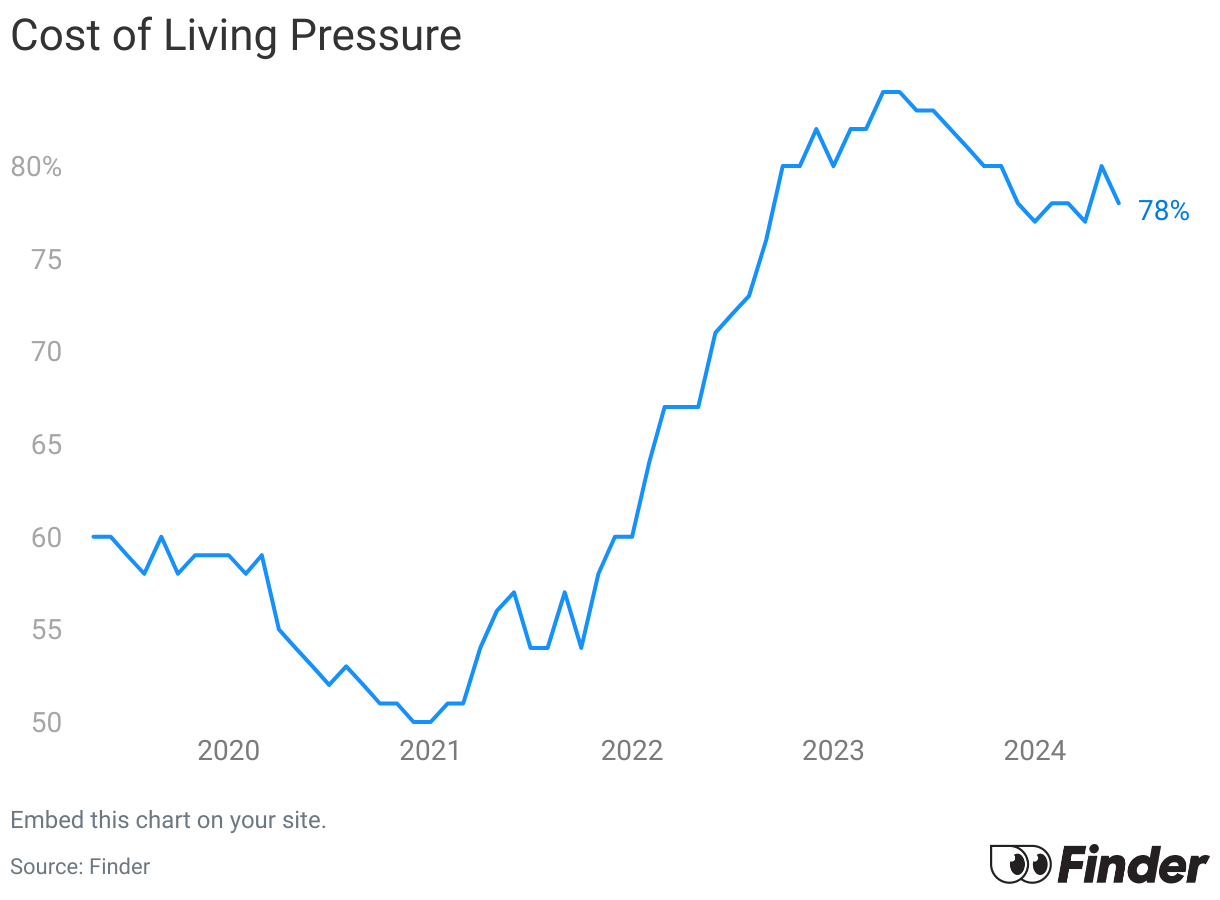

The Cost of Living Pressure Gauge, devised by Finder, measures the financial burden on Australian households. It integrates findings from Finder's Consumer Sentiment Tracker with official government data, providing a clear depiction of the economic challenges faced by consumers. Updated monthly, the model combines monthly and quarterly data on various aspects such as housing stress, salary projections, household debt, financial strain, savings, holiday intentions, credit card expenditure, the RBA cash rate target, property values and inflation. Presently, the Cost of Living Pressure Gauge stands in the very high range, at 77%.

So what exactly does this look like in raw terms?

At a very high pressure level of 77% at the end of December 2025:

Mortgage stress affects 56% of mortgage holders, an increase from 55% last month. However, 60% of renters are experiencing rent stress, a decrease from 61% last month.

Homeowners struggling with mortgage payments increased to 39% from 37% last month. Meanwhile, 46% of renters are still struggling to pay rent, down from 47% last month.

On average, Australians have $50,370 in cash savings, up from last month's $38,552

75% of Australians feel extremely or somewhat stressed about their finances.

The RBA's cash rate target is 3.60% as of January 2026.

Annual inflation increased by 3.4% in November 2025.

Australian credit card spending reached a record $40.1 billion in November 2025.

47% of the total credit card balances were accumulating interest.

Almost one in three (27%) Aussies are saying they can't handle their finances without a credit card.

Comparatively, at a moderate pressure level of 81% in December 2022:

Mortgage stress affected 56% of mortgage holders, while 51% of renters were stressed about their rent.

Only 33% of homeowners had difficulty paying their mortgages, while 46% of renters struggled to pay their rent.

On average, Australians had $31,625 in cash savings in December 2022.

79% of Australians said they were stressed about their current financial situation.

The cash rate target was lower at 3.10%

Annual inflation stood at 7.3%% in October 2022

In December 2022, the total Australian credit card spending was $32.55 billion.

46% of the total credit card balances were accumulating interest.

27% of Australians were saying they can't manage their finances without a credit card.

The December pressure reading shows a continued decline from April 2023's peak of 84%. This reduction is largely due to an increase in total savings and decrease in housing stress reported by consumers via our Consumer Sentiment Tracker. Additionally, there has been a reduction in unpaid credit card balances, as reported by the RBA. Nevertheless, the pressure remains significantly higher than the levels observed throughout most of 2020 and 2021. More information on the methodology behind these figures is provided below.

Methodology

Finder's Cost of Living Pressure Gauge merges data from its Consumer Sentiment Tracker (CST) and the Reserve Bank of Australia (RBA). Updated monthly, it combines CST data with RBA figures, which are updated either monthly or quarterly. When specific monthly RBA data is unavailable, the preceding quarter's figures are used.

Percentage data in the gauge has a set maximum, or "ceiling", defined as 100% pressure. For example, if a survey question like "How stressed are you about your financial situation?" has an 80% ceiling, then 80% of negative responses (extremely or somewhat stressed) equates to 100% pressure. Responses exceeding this ceiling are capped at 100%. This weighting is applied proportionally. Non-CST data is converted to a percentage as described below in "Data categories explained". After calculating all data, a global weighting is assigned to each figure, as outlined in the table below. Historical pressure figures may be revised if new historical data is released.

Data categories explained

Mortgage/rent stress: Percentage of consumers who identify their mortgage or rent payments as a primary financial stressor.

Mortgage/rent struggle: Percentage of consumers who find it difficult to make their rent or mortgage payments.

Salary sentiment: Percentage of Australians expecting a pay rise within the next year.

Spend sentiment: Percentage of Australians unhappy with the amount they need to spend monthly to maintain their standard of living.

Household debt sentiment: Percentage of Australians who have negative feelings about the level of household debt.

Financial stress: Percentage of Australians who report feeling extremely or somewhat stressed about their finances.

Credit card dependency: Percentage of respondents relying on credit cards to manage their finances.

Holiday plans: Percentage of Australians intending to go on a holiday in the upcoming year.

Savings index: Average monthly savings as a percentage of $1,000 of income.

Total savings index: Average total savings as a percentage of $50,000.

Cash rate index: Current cash rate relative to a 5% benchmark.

Savings rate index: Current average savings account interest rate relative to a 5% benchmark.

Credit card spend index: Total credit card spending as a percentage of a $35 billion benchmark.

Graham Cooke is Finder’s Head of Consumer Research, overseeing data analysis on consumer spending and saving habits. He is a passionate advocate for financial literacy and consumer rights, regularly appearing on major TV networks like ABC News and 7 News, and contributing to top outlets like Yahoo Finance and Money Magazine. Graham holds a Bachelor of Science (Hons) in Physics, as well as Tier 1 and Tier 2 certifications (RG 146) that comply with ASIC standards.

See full bio

Graham's expertise

Graham

has written

58

Finder guides across topics including:

Home loans and the housing market

Credit cards & personal finance

Finder Awards

Retail economics & FMCG

Travel

Finder's RBA Cash Rate Survey, Consumer Sentiment Tracker, Cost of Living Pressure Gauge and Property Investment Index

Discover average home loan sizes around Australia and much more with our comprehensive guide to home loan statistics.

Important information about this website

Finder makes money from featured partners, but editorial opinions are our own.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

The information provided by Frankie is general in nature and has been prepared without considering your objectives, financial situation or needs. Frankie may make mistakes so it's important that you review the information before deciding. By messaging Frankie, you agree to our Terms and have read our Privacy Policy.