Cover medical expenses if you prefer private healthcare

Pay for a nurse if you need home care

Afford everyday items, such as groceries and utility bills

Make sure your family will be okay without your income

A financial adviser or insurance broker can help you understand which insurance options are best for your needs.

Life insurance explained

Life insurance provides your family with an agreed-upon sum of money in the event of your death or, in some cases, if you are diagnosed with a terminal illness.

Sometimes called death cover, this type of insurance acts as a financial safety net for your loved ones when you die. It means, if the worst happens, your loved ones will still be able to afford the mortgage and pay off any debts. Getting through an illness or grieving for a loved one is hard enough without money worries on top.

Moneysmart.gov.au said that 91.5% of all claims for direct life insurance were paid out in the 12 months to 30 June 2021. There were just 16.9 policy disputes per 100,000 lives insured.

Life insurance is often used as an umbrella term to describe lots of different types of personal insurance. You can either buy a standalone policy or bundle several policies together to create cover that is perfectly tailored to you and your family.

Total and permanent disability (TPD) pays a lump sum if you are rendered totally and permanently disabled due to injury or illness. In some cases, it will pay a smaller lump sum if you are partially disabled.

Income protection pays a monthly benefit if you are unable to work due to illness or injury. Usually, it will only pay up to 75% or 85% of your typical wage.

Funeral insurance pays a lump sum to your family when you die, which they can use to cover the cost of your funeral.

Which types of life insurance are right for me?

It's possible you'll want more than 1 type of life insurance, so you can have peace of mind that you'll be covered in different situations.

If you're unsure which type, or types, are right for you, start by focusing on your motivation for buying life insurance.

I want to make sure my family will be okay if I die.

Life insurance/death cover might be right for you.

I want to make sure I can maintain my lifestyle if I can't work for a while.

Income protection insurance might be right for you.

I want financial help if I suffer a serious injury or critical illness.

Trauma insurance or personal accident insurance might be right for you.

I want to be able to cope if an injury or illness stops me from ever working again.

TPD insurance might be right for you.

I don't want my family to have to pay for my funeral.

Funeral insurance might be right for you.

I already know that my family and I will be fine no matter what happens.

You may not need life insurance at all.

Remember: You can mix and match different types of life insurance to create a cover perfect for you and your family. For example, combining death cover with income protection means you're protected if an injury or illness stops you from working, plus your family will also be protected if you die.

How do I buy life insurance in Australia?

There are 3 ways to get life insurance in Australia: direct, retail and super. Each option has its own pros and cons. Check them out below to figure out which way might be best for you.

Life insurance from super funds is usually less comprehensive than that offered by insurers so there's no harm in getting both. However, if you do already have life insurance in your super, you may want to choose a smaller amount of coverage from an insurer.

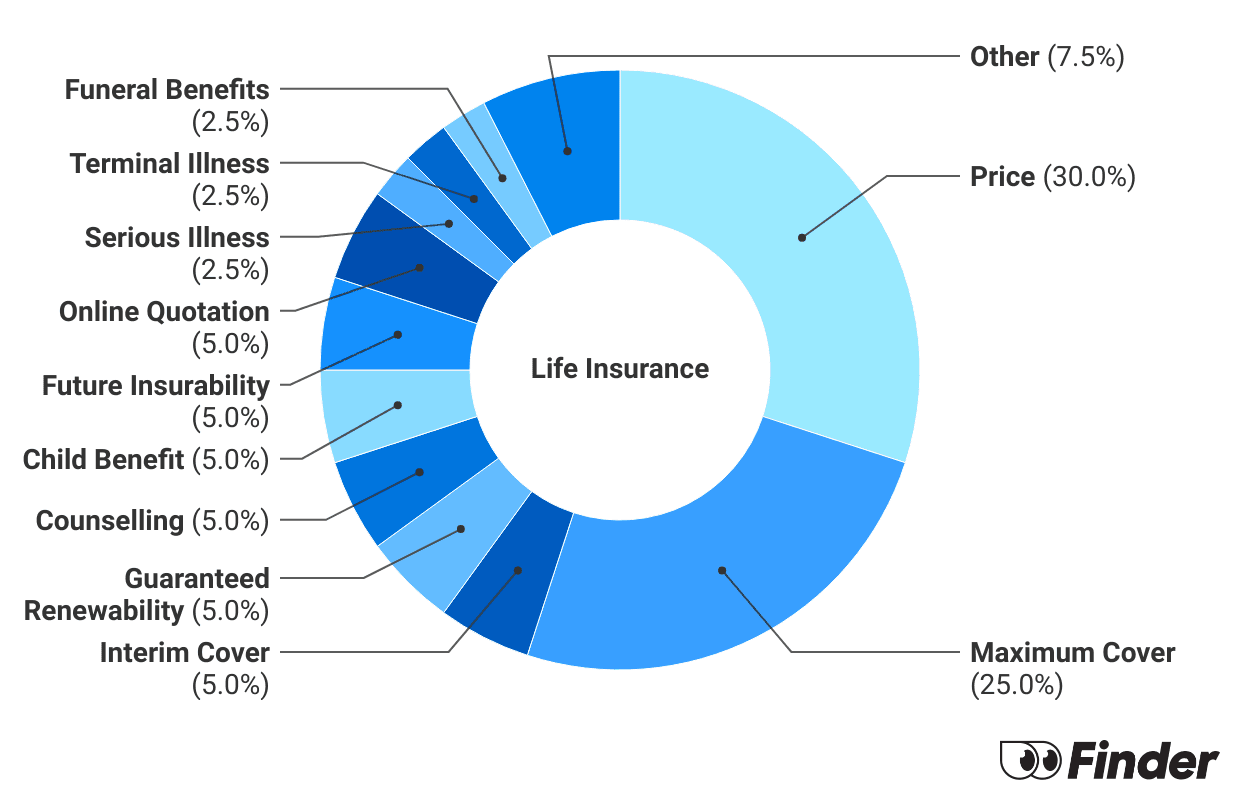

We've reviewed 21 Australian life insurance providers on the market, rating them a score out of 10 based on the features that each one offers. Here were the top 5 highest-scoring providers for features:

Did you know? Finder surveyed 5,050 Aussies and found that 19% already had income protection insurance while a further 13% plan on getting it.

What affects the cost of life insurance?

Lots of different factors influence the cost of life insurance. That's why it's important to get a personalised quote before deciding whether it's right for you.

Factor

Impact

Age

Younger people will pay less for life insurance

Biological sex

In general, women pay less for life insurance but more for income protection

Profession

People with riskier jobs will pay more for life insurance

Smoking

Non-smokers will enjoy cheaper life insurance premiums

Overall health

People without pre-existing medical conditions may pay less

Cover amount

The higher the potential benefit, the higher the monthly premiums

Is life insurance right for me?

If you answer YES to any of these questions, you should seriously consider life insurance:

Are you the main breadwinner for your family?

Would your family struggle to survive financially without your income?

Do you have financial obligations, such as a mortgage, rental agreement or car loan?

Do you have significant household debts?

If you answer NO to any of these questions, you should seriously consider life insurance:

Do you have significant cash savings that could last many years?

Do you have income streams that would continue after your death?

Do you have any high-value assets, such as a second home?

Could your family comfortably survive on your partner's income?

Did you know? Savings are scarce. A Finder survey revealed that the average Aussie has just $28,186 in cash savings.

How much life insurance should I get?

There's no perfect amount. You have to consider a lot of different factors when deciding how much life insurance you should get, such as:

How much cash savings you have

If you have passive income streams

What financial obligations you have

How many people are dependent on you

Your typical income and outgoings

How much is in your super fund

What other assets you have

Your level of household debt

How much help is available to you

How old you are

We created a calculator to help you figure it out. However, you should only use this as a starting point. If you want expert advice, you should speak to an adviser.

When will life insurance pay out?

Life insurance is there to help when things get hard. Take a look at the situations below to see which type of policy would pay out.

Did you know? Most people can get life insurance. In a Finder survey of 5,050 Aussies, only 2% had been refused cover by a life insurer.

Life insurance glossary: Key terms to know

A rundown of the tricky definitions for life insurance. Plus, what to look for when you're comparing.

Beneficiary

The person you've nominated to receive your life insurance payment if you pass away or become terminally ill. You can nominate anyone as your beneficiary. There can be more than one beneficiary and each beneficiary can receive different amounts.

Children's insurance

Covers your child for death, terminal illness or a serious injury or illness that's specified in your policy. Typically, children's cover needs to be added as an optional extra.

Finder looked at 16 policies on our database and found just a few give you the option of adding a child to a policy.

Cooling-off period

The amount of time in which you can cancel your policy after signing up – and get a full refund of any premiums paid. The vast majority of insurers offer a cooling-off period of up to 30 days.

Counselling benefit

Some insurers will pay costs for grief counselling sessions for you or your partner. Counselling benefits usually have a limit of around $1,000. It can be claimed after a death or terminal illness claim.

Exclusion

An exclusion is any specific risk or event that you can't claim for under your policy. Insurers can apply exclusions to certain pre-existing medical conditions. For example, they may not cover any claims related to mental health.

Exclusion period

How long you'll have to hold your insurance before a policy exclusion turns into a claimable event. For example, it's common for suicide to have a 13-month exclusion period.

Fully underwritten

With a fully underwritten life insurance policy, your application is assessed upfront. Whereas a policy that isn't fully underwritten is assessed at the time of a claim.

Pays a lump sum benefit – usually up to $15,000 – so your loved ones can meet the cost of your burial or cremation without using their own money.

You could look for a funeral policy offering a guarantee that any payout won't be less than the total you've paid in premiums. This is sometimes called a premium guarantee.

Guaranteed acceptance

You can get insurance without having to answer any health questions, or take a medical exam or blood tests.

Guaranteed acceptance policies, also known as auto-acceptance policies, will have an age eligibility requirement. This can range between 16 and 80 years of age.

Guaranteed Renewability

The insurer lets you renew your coverage each year, as long as you keep paying for your premiums. Many life insurers in Australia offer this peace of mind.

Income protection insurance

Income protection insurance pays a monthly wage if you need to take time off work due to a sudden accident or illness. Many insurers will pay up to 70% of your pre-tax income.

Inflation protection

This ensures your premiums keep up with inflation so that your amount of cover is worth as much by tomorrow's dollar. You can ask your insurer to switch off this automatic policy feature, but it could leave you underinsured.

Interim accident cover

Insures you while your life insurance application is being underwritten or waiting to be approved. Typically, interim insurance will cover you for up to 90 days.

Joint life insurance

A policy that covers 2 people, but it pays out one time. A lump sum goes to the other policyholder in most cases.

Joint life insurance can be a cheaper option than two single policies. But it's potentially complicated if a relationship ends.

Level premium

Your insurance generally won't increase in price as you get older. You'll usually pay more in the beginning but they offer more certainty over time. Only a few direct insurers in Australia offer level premiums.

Loading

Essentially, you have to pay a bit more to include your health condition, job or hobby in your policy. Any loadings will be offered during the life insurance application process.

Minimum cover

The smallest amount of insurance (or, sum insured) you can take out. Many insurers in Australia set a minimum cover level of $100,000.

Maximum cover

The cover limit offered by an insurer. It's the most you can be paid out after a claim. Maximum cover limits can range from $500k to $25 million. TAL told Finder it had "no set limit" for a payout.

Maximum entry age

The maximum age you can be to apply for life insurance. Common age caps are 64 or 65, but some providers go up to 70+.

Some insurers will require you to have a physical examination before you're approved; others will just need you to answer questions about your medical history on your application form.

Monthly benefit

A regular monthly payment if you're unable to work due to illness or injury. It's designed to replace a portion of your regular income. Monthly benefits are a common feature of income protection policies.

Mortgage protection insurance

Insurance that can cover your mortgage repayments if you have a serious illness or pass away. Mortgage protection will only cover your mortgage repayments, not all the other bills you'd need to pay if you lost your ability to earn an income.

Personal accident insurance

Insurance to replace your income if you are temporarily unable to work after an accident. This cover can be bought as a standalone policy. Keep in mind it won't cover you if you get sick and can no longer work.

Personal insurance

An umbrella term for the following 4 core types of life cover: Life insurance, Total and permanent disability (TPD) insurance, trauma insurance and income protection cover.

A condition you have, or have had, prior to taking out life insurance.

You may be able to get life insurance that includes cover for a defined medical condition. It's likely to cost you more. However, if an insurer thinks your condition is too high risk or isn't under control, they'll exclude it from your policy.

Premiums

The amount you pay an insurer for your cover. Premiums can be paid weekly, fortnightly, monthly or annually.

A policy option that lets you stop paying premiums entirely. You will typically lose all your cover while your policy is suspended.

Not all life insurance policies include a suspension of cover benefit. Check with an insurer directly.

Premium freeze

A premium freeze lets you stop your premiums from increasing as you age.

It's only available with stepped premium policies because the cost rises with age. By activating a premium freeze, your level of cover will drop over time.

Retail life insurance

Buying life insurance through a broker, who will give you tailored advice on securing cover. Buying a retail policy is one of 3 ways to get life insurance in Australia. The others are directly with an insurer or through your superannuation.

Salary continuance

You can receive up to 75% of your regular earnings each month to cover general living expenses if you can't work due to an accident, illness or injury

Salary continuance insurance is held within a super fund, and you'll pay your insurance premiums from your super balance rather than directly from your bank account.

Typically, to be classed as a 'non-smoker' you'll need to be free of any smoking products for 12 months, but this can vary between insurers.

Stepped premiums

How much you pay for your policy increases each year by a certain percentage. Most policies in Australia have stepped premiums. Yearly increases can range from 2% to 7%.

Term cover

A type of life insurance that provides a set amount of cover for a set amount of time (or, 'term'). The maximum cover offered by term policiescan range from $100,000 to $1 million.

Terminal illness benefit

An insurance which pays out a lump sum if you're diagnosed with an illness which cannot be cured, such as advanced cancer. Benefits can range from around $1 million to as much as $25 million in Australia. It's usually included with a life cover policy.

Total and permanent disability (TPD)

An insurance that pays a lump-sum (as high as $5 million) if you get sick or injured and become permanently disabled. In most cases, TPD cover is available as an add-on when you take out life insurance.

Trauma insurance

A type of insurance that pays out if you are diagnosed with a critical illness or suffer a life-changing injury that's listed in your policy. Examples can include cancer, heart attack and stroke. Trauma insurance pays up to $2 million as a lump sum.

Underwriter

When you apply for cover, the insurance underwriter assesses your level of risk and determines whether the insurer should offer you cover, as well as under what conditions that cover should be offered.

You could check to see if a policy has been underwritten by a major insurer, backed by many years of experience.

Want to know more about life insurance?

Buying life insurance can be a tricky decision. Luckily, we have heaps of guides that can help.

If you have any lingering questions about insurance premiums, we break down the different payment structures you can have. Find out if stepped or level premiums are the way to go.

If there's anything you still have questions on, drop us a comment below and we'll reply to you.

Life insurance frequently asked questions

Life insurance is a type of insurance that offers financial help to your loved ones if you die or are diagnosed with a severe illness. Typically, it offers a lump-sum payout to meet the cost of debts, such as your mortgage, bills and other living expenses.

Yes. Some life insurance policies will have an expiry age. However, the specific age varies between different insurers and types of life insurance. Always check the product disclosure statement (PDS).

Yes. Currently, life insurance providers don't specify COVID-19 exclusions on individual policies. This means if you're one of the very unfortunate people who die from COVID-19, your policy should pay out. However, Moneysmart.gov.au advises you should "check if the policy will cover you for claims associated with COVID-19" before you buy, renew or switch insurance.

Claims for certain high-risk activities or illegal ones such as drug use won't be covered by life insurance. You also can't make a claim linked to a pre-existing condition that you failed to disclose during your application.

To learn about more common policy exclusions that apply to life insurance, read the "general exclusions" section of a policy's PDS.

With income protection, there'll be a fixed time you'll need to be off work for your policy to start gaining a benefit. This is known as the waiting period. It usually ranges from 14 days to 2 years. Generally, a longer waiting period will mean a cheaper premium.

Aside from death cover, other types of life insurance that provide financial security if you are injured or become too sick to work include the following:

Income protection insurance. Pays a replacement income if you're temporarily unable to work due to illness or serious injury.

Trauma insurance. Pays a lump sum if you're diagnosed with a critical ilnness, such as cancer.

A life insurance payout goes to the beneficiary, which is the person or people you choose to receive the financial benefit of your life cover policy after you die. A beneficiary can be a family member, a friend, a trust or an organisation.

We can't say which is the "best" policy as it depends on the insurance type that meets your specific needs and life circumstances. That said, we've identified some of the highest-scoring life insurance brands based on our most recent Finder Awards data.

Technically, there's no limit to the number of life insurance policies you can have. Some choose to mix and match policies to get coverage that works better for them. However, many prefer to have multiple benefits baked into a single policy, which is easier to manage.

Yes, it is possible. If you have a pre-existing medical condition, there are insurers who will still cover you. But they might ask you to pay slightly higher premiums or exclude that condition from your cover. It's really important to disclose any condition you have when you apply for life insurance. Not doing so could void your cover.

Child life insurance is a feature you can add to your life insurance policy for an added fee. It will pay out a financial benefit if your child dies or suffers a serious medical condition. We reviewed 15 policies on Finder and only 3 brands – Real Insurance, Guardian and Kogan – offer child cover as an extra.

No. Life insurance will only pay out if you suffer a serious medical condition that's listed in your policy, or if you pass away.

While life insurance can be cancelled at any time, keep in mind if you cancel your insurance and decide to take it out later, you'll likely have a higher premium. That's because insurers will see you as a higher risk due to your age or any further medical conditions you may have had.

Nicola Middlemiss is a contributing writer at Finder, with a special interest in personal finance and insurance. Formerly a business and finance journalist, Nicola has written thousands of articles helping Australians better understand insurance and grow their personal wealth. She has contributed to a wide range of publications, including Domain, the Educator, Financy, Fundraising and Philanthropy, Insurance Business, MoneyMag, Mortgage Professional, Yahoo Finance, Your Investment Property, and Wealth Professional. Nicola has a Tier 1 General Insurance (General Advice) certification and a Bachelor's degree from the University of Leeds. See full bio

Nicola's expertise

Nicola has written 232 Finder guides across topics including:

Personal finance

Personal insurance, including car, health, home, life, pet and travel insurance

We asked hundreds Australians how satisfied they were with their crypto trading platforms. Here's what they told us.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

Important information about this website

finder.com.au is one of Australia's leading comparison websites. We are committed to our readers and stands by our editorial principles

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product. You can learn more about how we make money.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.