High risk car insurance

Getting car insurance for a high risk driver can be possible, it just depends on the offence and how long it's been. Read about your options below.

Largely, people are considered high risk drivers because they’ve:

Most likely but it’ll depend on why you’ve been deemed a ‘high risk’ driver and how long ago any offences occurred.

In some cases, the insurer will decide you’re risky and up your premium. This is particularly true in the case of younger drivers, high mileage drivers, those with prior at-fault claims, and those with speeding fines.

In other, more serious cases, they'll decide you’re too risky and refuse to cover you. This is particularly true for those with DUIs, licence suspensions and criminal records. However, not all insurers are created equal and we’ve found a bunch who may cover you for some of these instances.

Every month, we source quotes from 11 car insurers in Australia. We answer "yes" when asked if the driver's licence has been "cancelled, suspended or restricted" due to any driving offence(s). Of the 11, we were only able to return quotes for 3 providers.

Keep in mind, whether you'll actually be able to get cover depends on your specific offence, individual circumstances and your risk profile.

| Brand | Annual cost | Apply |

|---|---|---|

| $1,946.26 | Get quote | |

| $1,919.81 | Get quote |

Prices accurate as of February 2026

We currently don't have that product, but here are others to consider:

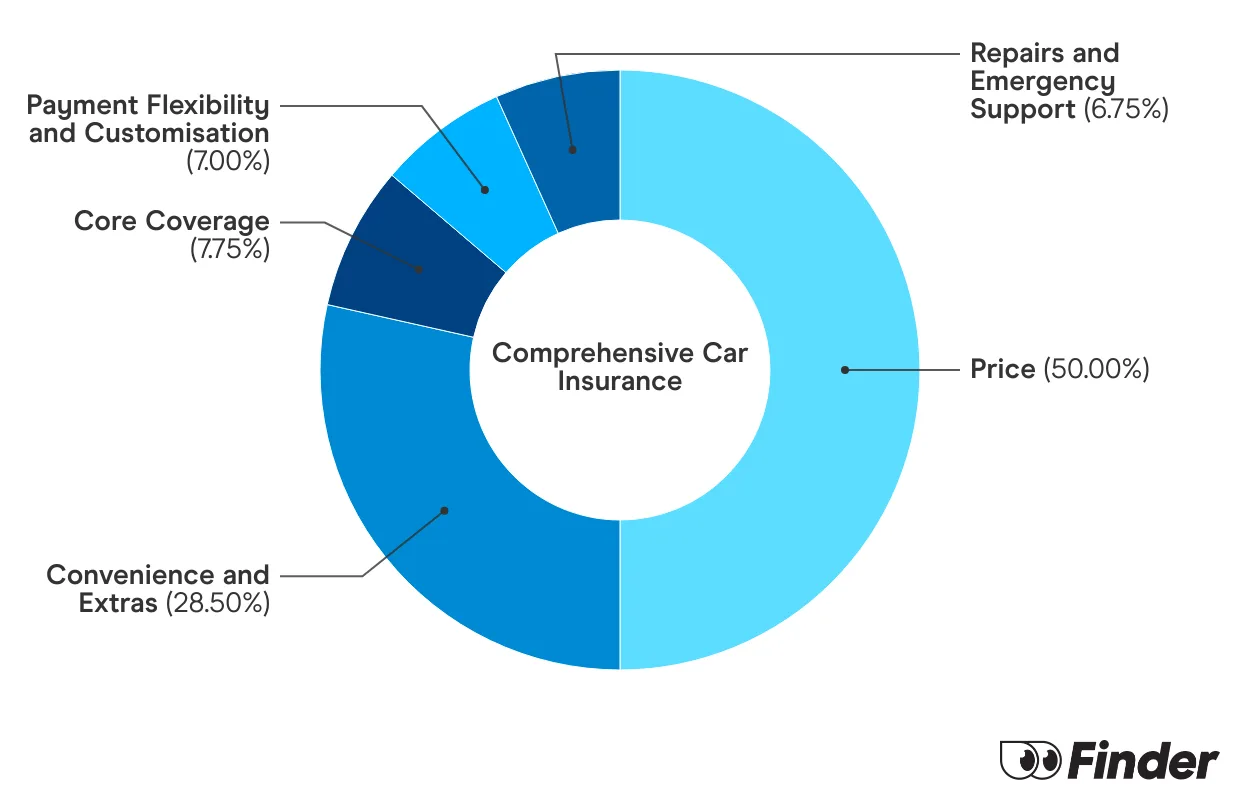

How we picked theseWe analyse over 30 car insurance products across insurance providers, and rate each one for price and features. We collect up to 36 quotes per product, for male and female drivers in New South Wales, Victoria, Queensland, South Australia, Tasmania and Western Australia. Quotes are collected for 20 year olds, 30 year olds and 60 year olds, assuming an excess of $850 for a 2020 Toyota Corolla 4 door sedan model, with an average 15,000 kms driven each year. While we are not allowed to display actual quotes, our Finder Score aims to serve as an indicative guide to how cost and feature competitive a product might be for you.

Our feature score assesses each product for more than 15 features across loss and damage coverage, repairs and assistance coverage, personal items coverage and policy coverage. Features we assess include but are not limited to legal liability, essential repairs, new car replacement, car hire events, roadside assistance, agreed or market value, windscreen damage and natural disaster coverage.

Depending on your answers to our car insurance quiz, we upweight the relevant price score or feature score to generate a dynamic Finder Score. Finder Score, Price Score and Feature Score are only to be used as indicative guides and are not product recommendations.

"I had my licence suspended at 18. It was only low range speeding, but NSW has a no tolerance rule for P-platers. As a result, I later had to cop higher car insurance premiums for like 10 years, as I was considered a high risk driver. I also had way fewer options, as a lot of companies wouldn't cover me at all. The only way I was able to save money was going with third party property damage cover rather than comprehensive. It was super frustrating but at least I had some level of cover."

| Response | Male | Female |

|---|---|---|

| Yes | 56.25% | 45.59% |

| No | 41.67% | 53.26% |

| I have never driven before | 2.08% | 1.15% |

Every month, we run quotes from 10 popular car insurance providers in Australia to see who might offer cover for drivers with an at-fault accident claim. To get our quotes, we chose “yes” when asked about a past accident claim and selected "at fault".

It’s worth noting, usually, insurers asked about offences in the last 3 or 5 years. So if your at fault claim is beyond then, you won’t need to list it.

The good news is, we were able to return quotes for all 10 providers. The bad news is, it’s a little expensive.

Remember, the below should be used as a guide only. Your own risk profile will differ and your own quotes will reflect your personal circumstances.

| Brand | Annual cost | Apply |

|---|---|---|

| $1,438.35 | Get quote | |

| $1,017.33 | Get quote |

| $1,119.07 | Get quote | |

| $2,105.68 | Get quote | |

| $2,456.93 | Get quote | |

| $2,116.26 | Get quote | |

| $2,594.69 | More info | |

| $1,068.21 | More info |

| $2,225.09 | More info | |

| $2,074.87 | Get quote |

Prices accurate as of February 2026

We currently don't have that product, but here are others to consider:

How we picked theseAs you’ll — rather painfully — know, getting car insurance when you’re deemed a high risk driver, can be expensive. Fortunately, there are plenty of ways to save that don’t rely on having a squeaky clean driving history. Here’s what you can do:

Here's a guide to getting affordable car insurance that will still cover the essentials.

Find out how to get your car registration transferred in Victoria.

Your guide to Blue Slips.

Your guide to demerit points and how they affect your car insurance.

Bank of Queensland car insurance offers three levels of cover, flexible premium payment options and a lifetime guarantee on repairs.

Find affordable and comprehensive car insurance for P-platers with this handy guide.

Compare the latest car insurance discounts and deals to save further on your policy or access bonus offers. Discounts up to 25% for purchasing online

Discover the steps to get affordable car insurance if you are under 25.

Explore our analysis and see how you can find the best car insurance for your needs.

Compare cover from a range of car insurance providers and find out some of the things you will be covered for under a comprehensive policy.